Tim Weinhold

Adam Smith probably tops history’s list of influential teachers with the most followers who largely misunderstood their teacher’s message. As we all know, Smith is widely viewed as the father of capitalism, based on his 1776 book, The Wealth of Nations. Smith and his book remain hugely influential to this day.

His principal thesis was that individuals – and enterprises and countries – should focus their productive activities on that which they do best, and then, via a free market, trade their specialised outputs for the goods and services produced by others. He argued that this combination of specialised production, with supply-and-demand-based free-market trading, most efficiently allocates productive resources and, as a result, maximises overall wealth creation. As well, it (generally) maximises utility for all participants; that is, everyone is better off.

Smith’s core contention, therefore, is that the market’s ‘invisible hand’ transforms self-interested production and trading behaviours into outcomes of maximum economic and social benefit. This has provided the foundational rationale for business and free markets – in other words for capitalism itself – ever since. Much of this is summed up in the book’s most famous sentence: ‘It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their regard to their own self-interest.’

Arguably no other single sentence has ever been so thoroughly misunderstood, by so many people, to such disastrous effect. In fact this misunderstanding goes to the heart of why so many are now so critical of contemporary capitalism. More specifically, it explains why the rewards of late-twentieth and twenty-first-century capitalism have flowed increasingly to the wealthy, while the fortunes of much of the (Western) middle class, working class and poor have deteriorated.

The misunderstanding arises from a failure to recognise that, morally and practically, there are two very different kinds of self-interested behaviour. One occurs when an individual – or enterprise – acts for their own benefit at the expense of someone else. We generally describe such behaviour as selfish and predatory. Fortunately, there is a quite different sort of self-interested behaviour – where someone achieves a favourable outcome for themselves and for the other individual(s) affected by their action.

Though both behaviours are self-interested, their effects are poles apart. The first unilaterally imposes costs on someone else, making them worse off; that is, they are harmed. The second, by contrast, benefits not only the one taking action but the other party as well.

It is not surprising, then, that from our toddler years on we experience being on the receiving end of these two behaviours very differently. Reflect back, for example, on your own toddlerhood. Suppose you had been playing with a favourite toy and your older sibling came by and snatched it away saying, ‘I want to play with this now!’ Not very hard to recall how you felt, right? A terrible injustice has been perpetrated! Call in the authorities (Mom or Dad)! Such a grave wrong, such a violation of all that is just and proper, must be put right – NOW!

Suppose, though, that your sibling had said, ‘I’d like to play with your toy now, so how about if I let you play with my super-duper new toy?’ Provided that the new toy in question really was super-duper, you probably would have been quite happy to accede. In both cases, the result for your sibling was the same – they got to play with the toy they wanted. But the respective outcomes for you are quite distinct: in one scenario you were disadvantaged (harmed); in the other you were made better off (helped).

If even a toddler instinctively understands the watershed difference between these two versions of self-interest, why, we might ask, has it proved so difficult for adults – specifically economists, business people, business academics, political commentators and the like – similarly to understand that difference when it comes to the way business, and capitalism, are meant to work?

Yet a great many of Adam Smith’s devotees find themselves unable to grasp that distinction. Over and over they evidence a belief that, effectively, Smith’s most famous sentence reads, ‘It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their selfishness.’ They believe that Smith was claiming for free markets and capitalism something quite extraordinary: that they magically transmute the lead of selfishness and exploitation into the gold of maximised benefit for individuals and society. This is nonsense and delusion.

And yet we find the Harvard economist Edward L. Glaeser declaring in The New York Times:

Two hundred and thirty years ago, Adam Smith made the case for selfishness when he wrote that ‘it is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own self-interest.’[1]

Or we read comments like this one, attributed to one of the two most influential economists of the twentieth century, John Maynard Keynes: ‘Capitalism is the extraordinary belief that the nastiest of men for the nastiest of motives will somehow work for the benefit of all.’[2] Keynes may simply have been paraphrasing an earlier quotation from a close colleague, E. A. G. Robinson, who wrote in his book Monopoly: ‘The great merit of the capitalist system, it has been said, is that it succeeds in using the nastiest motives of nasty people for the ultimate benefit of society.’[3]

Of course, no one has done more to associate capitalism with selfishness – and its close corollary, greed – than Ayn Rand. Then again, in her full-on defence of selfishness and greed, maybe she meant something different from what we imagine. Rand acknowledged, for instance, in the introduction to her book The Virtue of Selfishness, that she was using the term ‘selfishness’ to mean, more precisely, ‘concern with one’s own interests’.[4] Hmmm.

Along similar lines, consider this defence of greed from the other most influential economist of the twentieth century, Milton Friedman:

Well first of all, tell me: Is there some society you know that doesn’t run on greed? You think Russia doesn’t run on greed? You think China doesn’t run on greed? What is greed? Of course, none of us are greedy, it’s only the other fellow who’s greedy. The world runs on individuals pursuing their separate interests … there is no alternative way so far discovered of improving the lot of the ordinary people that can hold a candle to the productive activities that are unleashed by the free-enterprise system.[5]

If smart, prominent commentators like these are going to treat ‘selfishness’ and ‘greed’ as synonyms for ‘self-interest’, no wonder so many devotees imagine Adam Smith claimed the market’s beneficent hand turns selfishness and greed into social and economic blessing. This has done great harm. In particular it has caused a great many business people to believe that selfish, exploitative behaviour, though toxic in every other arena of life, is somehow magically beneficial when practised in business.

But failing to distinguish the words ‘selfishness’ and ‘greed’ from ‘self-interest’, as sloppy and unhelpful as that may be, is not our real problem. Rather, the words themselves focus our attention in the wrong direction – towards the character and motivation of the actor. As a result, they keep us from recognising what truly differentiates good from bad and moral from immoral behaviour.

Let’s revisit for a moment our hypothetical scenario from your toddlerhood. When your sibling wanted your toy, your response had nothing to do with his or her motivations or character. If your sibling’s behaviour injured you – made you worse off – then you knew you had been mistreated and a wrong perpetrated. Period. If, instead, their action left you better off, you were happy to approve their behaviour – whether or not they were motivated by self-interest, selfishness or greed.

You knew your sibling’s conduct was wrong, or not, entirely based on the effect it imposed on you. Which means that, even as a toddler, you were thinking clearly as to what actually differentiates behaviours that are good from bad, right from wrong, moral from immoral; and that you were already thinking clearly about how we should assess good versus bad business conduct, and the difference between moral versus immoral versions of capitalism.

Of course, there’s more here than the justice instincts of toddlers. Throughout human history – across religions, across civilisations, even now in our post-religious Western secularism – one principle has always provided the bedrock foundation for human morality: the golden rule – ‘Treat others as you yourself wish to be treated’; or in its alternative rendering – ‘Love your neighbour as yourself.’ Notably, this cornerstone moral principle zeroes in on our actions – how we actually treat others – not our motivations.

Just as notably, the golden rule envisages a behavioural landscape comprised of not two but three impact categories – two of which meet the golden rule test. One such behaviour/outcome occurs when an individual – or enterprise – chooses to do good for someone else to their own detriment. We typically refer to such behaviour as altruism or selflessness. More precisely, though, we can label this ‘lose–win’ behaviour. The one taking action is disadvantaged for the sake of benefiting another.

Most of us have a tenuous relationship with selflessness. We acknowledge its moral attractiveness yet practise it infrequently. There are exceptions, of course. Many parents exhibit a great deal of lose–win behaviour towards their children. Good soldiers in combat may do so as well. And good spouses. Nevertheless, selflessness seems more the province of saints like Mother Teresa than us ordinary mortals. Across the landscape of human behaviour it is decidedly more the exception than the rule.

Fortunately there is another behaviour/outcome that also fulfils the golden rule. Win–win behaviour, as noted earlier, occurs when someone’s conduct brings about a beneficial outcome for themselves and for the other individual(s) affected by their action. Such behaviour is almost always motivated by self-interest. Yet it entirely meets the ‘Love your neighbour as yourself’ moral test.

Selflessness, therefore, is not the only way to keep the golden rule. Self-interested actions also meet the test for good and moral behaviour — provided they don’t come at the expense of others. It’s only when self-interest crosses over from win–win behaviour into win–lose territory that it violates the golden rule and becomes what most of us call selfishness (Ayn Rand and certain economists notwithstanding). A simple summary diagram should prove helpful (see Figure 1).

A great deal of what passes for moral commentary, at least as it relates to business and economics, assumes the important moral watershed is between selflessness and selfishness (or self-interest) – as if the foundational injunction is to ‘Love others rather (or more) than yourself.’ This both misunderstands the golden rule and misses the moral divide of real consequence.[6]

In fact the line of first-order significance is that between win–win mutuality and win–lose selfishness. It is here that we find the precise divide between what is moral and immoral, the exact boundary between right and wrong. It is also the difference between good and bad outcomes or, more broadly, between blessing and blight. More prosaically it is the difference between the merchant who makes money by providing a beneficial product and the mugger who takes money at knifepoint – or the loan shark (or payday loan company) who does so via extortionate interest. One practises a morally commendable self-interest, while the others’ behaviour is morally reprehensible.

As a moral philosopher, Adam Smith understood this distinction clearly, even if many of his followers do not. In his book The Big Three in Economics: Adam Smith, Karl Marx, and John Maynard Keynes, the prolific economics author Mark Skousen describes Smith’s fundamentally moral understanding of self-interest:

Smith recognized that people are motivated by self-interest. It is natural to look out for one’s self and one’s family above all interests, and to reject this would be to deny human nature. Yet at the same time, Smith did not condone greed or selfishness. For Adam Smith, greed and selfishness are vices.[7]

Skousen elaborates Smith’s morally circumscribed view of self-interest in a piece for the Foundation for Economic Education:

[Smith] wrote eloquently of the public benefits of pursuing one’s private self-interest, but he was no apologist for unbridled greed. Smith disapproved of private gain if it meant defrauding or deceiving someone in business. To quote Smith: ‘But man has almost constant occasion for the help of his brethren … He will be more likely to prevail if he can interest their self-love in his favour … Give me that which I want, and you shall have this which you want, is the meaning of every such offer.’ In other words, all legitimate exchanges must benefit both the buyer and the seller, not one at the expense of the other.

Smith’s model of natural liberty reflects this essential attribute: ‘Every man, as long as he does not violate the laws of justice, is left perfectly free to pursue his own interest his own way, and to bring both his industry and capital into competition with those of any other man, or order of men.’[8]

All of which makes especially compelling Smith’s pithy, emphatic statement of what we might call the ‘foundational justice dictate’ in his earlier (1759) masterwork, The Theory of Moral Sentiments: ‘There can be no proper motive for hurting our neighbour.’[9] It would be hard to misinterpret that.

The bottom line is this: Adam Smith, the father and foremost apologist for self-interested capitalism, nevertheless saw a bold bright line between actions that benefit both us and our neighbour versus those that help us but harm our neighbour. He recognised that a self-interested win–win mutuality was essential to business success and the creation of wealth, yet never countenanced win–lose selfishness and predation. He knew that taking advantage of others for one’s own benefit is both deplorable and dangerous. Smith understood clearly (along with virtually every other moral thinker throughout history) that such predatory behaviour undermines the very foundation of human society – and deserves to be roundly condemned by all.

This is consequential for three key reasons:

During the middle portion of the twentieth century, American business was the envy of the world. American corporations were the pre-eminent global leaders in virtually every industry. And the prevailing view among CEOs and business academics was that the purpose of a corporation was to create value for several different constituencies, more or less in this rank order: customers, employees, host communities, society and shareholders. In practice this meant companies generally aimed at win–win outcomes vis-à-vis their various stakeholders.

But starting in the 1970s, American business embraced an entirely different conception, a view that the pre-eminent purpose of a corporation is to maximise the wealth of its owners.[10] This view, labelled ‘shareholder value maximisation’ (SVM), has been the prevailing consensus ever since.

This watershed reconception of business purpose was first advanced by Milton Friedman in his famous 1970 opinion piece in The New York Times Magazine entitled, ‘The Social Responsibility of Business is to Increase its Profits’.[11] Then in 1976 two business academics, Michael Jensen and William Meckling, published ‘Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure’.[12] This hugely influential article argued for giving CEOs substantial grants of stock, or stock options, to better ensure their energies were pointedly focused on behalf of shareholders.

But it was in the 1980s when business people themselves embraced in a big way this new understanding of corporate purpose. They were especially influenced by Jack Welch’s 1981 speech, ‘Growing Fast in a Slow Economy’, in which he made clear that, henceforth, General Electric’s primary objective would be to return maximum value to shareholders.[13] This conception of corporate purpose has reigned supreme in America ever since. (It got considerable, but less, traction in other English-speaking countries, and relatively little in Europe.)

In practice, SVM has translated into a rigorous focus on maximising short-term profits. But maximising one outcome necessarily means sacrificing others. So when profits conflict with creating value for customers (or with the good of employees, suppliers, host communities or even society as a whole), SVM dictates that profits prevail.

In fact this understates the distorting effect of SVM. Once corporate purpose is defined in terms of immediate maximised wealth for shareholders, the priority job of senior management becomes channelling every dollar possible away from employees, suppliers, communities, society, even away from research and development for future growth – all for the sake of a fattened bottom line this quarter or next. SVM represents, therefore, a giant turn towards selfishness, towards advantaging business owners – senior management owners in particular – at the expense of everyone else.[14] Consequently a great many businesses have moved squarely into the win–lose, plunder and predation end of the moral landscape.

The effects have been severe. Rather than a last resort, layoffs are now a go-to choice to boost near-term profits. Pension plans have all but disappeared. For many retail workers, so too have predictable hours and incomes. More and more health care cost has been pushed from employers to employees. At a more foundational level, the ‘gig economy’ threatens to undo the entire landscape of worker protections, blithely turning employees into contractors with virtually no rights or security. And maybe most significantly, the share of economic output flowing to profits (shareholders) is at an all-time high, while the proportion flowing to workers has never been smaller (see Figure 2).[15]

Of course, corporate win–lose predations are hardly restricted to employees. Anti-customer corporate scandals – GM’s ignition switch, VW’s emissions cheating, Wells Fargo’s bogus accounts, Wall Street’s seemingly endless stream of malfeasance – have become commonplace. So has corporate tax avoidance, including through domicile inversions and aggressive use of tax havens.

And what about unilaterally pushing business costs onto taxpayers? As a rather notable instance, American taxpayers spend in the vicinity of $8 billion a year providing poverty assistance benefits to Walmart workers[16] – despite the company topping the 2016 Fortune Global 500 with revenues of $482 billion. And, of course, there’s this egregious example of misbehaviour: less than a decade ago the greed and recklessness of our largest financial institutions came within a hairsbreadth of taking the entire global economy over the cliff.

No wonder the ranks of capitalism’s critics continue to swell, as does the vehemence of their critiques. No wonder more young people now say they prefer socialism to capitalism (43 per cent to 32 per cent).[17] No wonder the communications group Edelman reported recently that the credibility of corporate CEOs has fallen ‘off a cliff’, dropping 12 points in just the past year.[18]

There is a better way. Business, practised wisely and well, is an extraordinarily powerful means for human betterment. Business fulfils this high calling by creating value for its stakeholders in two particular and important ways. First and foremost, business solves human problems. In fact it solves an especially large and important set of human problems: the material challenges of human existence.

Virtually every product and service offered by business is meant to meet a material human need.[19] In some cases business products may represent novel and dramatic new solutions to those needs (breakthroughs), as happened with the invention of automobiles, personal computers and mobile phones. In other cases the solutions may be more modest: a less expensive option for air travel, a more comfortable mattress or a non-polluting laundry detergent. All of which makes business, quite literally, a solutions machine targeted at humankind’s material welfare.

But business creates an entirely different type of value as well. When a business sells its products for more than their cost of production, it creates profit – and thereby enlarges human wealth. Provided this wealth is broadly deployed rather than narrowly hoarded, business both solves human problems and creates the economic provision that makes those solutions affordable and accessible.

Both forms of value creation are extraordinarily important. As Eric Beinhocker and Nick Hanauer note in their compelling article, ‘Capitalism Redefined’: ‘Ultimately, the measure of a society’s wealth is the range of human problems that it has found a way to solve and how available it has made those solutions to its citizens.’[20] It is no overstatement, therefore, to say that business provides the material foundation for human flourishing.

Or, more precisely, business is capable of providing the material foundation for human flourishing. It delivers these great benefits when, and to the degree that, it engages in win–win behaviour. Period. But win–lose behaviour is an entirely different matter. When business selfishly and narrow-mindedly pursues profits at the expense of stakeholders, then it becomes something altogether disparate. Rather than a means of value creation, it becomes a mechanism for value extraction – in other words, for plunder and stealing. That version of business – based on the intrinsically selfish ideology of shareholder value maximisation – rightly deserves the ire and condemnation increasingly directed against it.

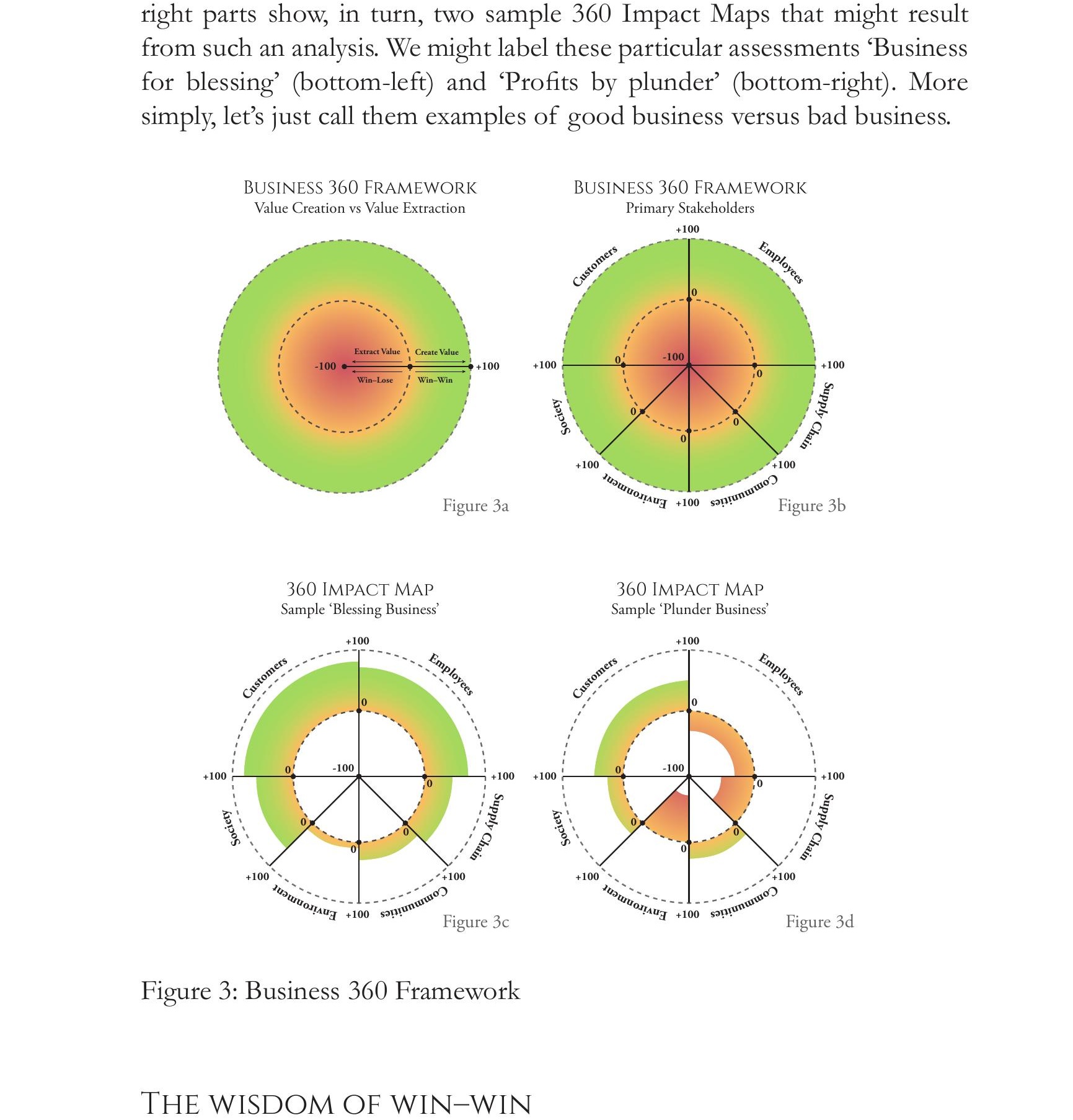

The Business 360 Framework[21] provides a helpful analytical tool by which to understand and apply all this in practice, as shown in Figure 3. The top-left part of this figure identifies the crucial difference between win–win behaviour that creates value for stakeholders, versus win–lose behaviour that extracts value, and provides a +100 to -100 reference scale. The top-right part lays the basis for applying this create-versus-extract value assessment to each of a company’s primary stakeholders. The bottom-left and bottom-right parts show, in turn, two sample 360 Impact Maps that might result from such an analysis. We might label these particular assessments ‘Business for blessing’ (bottom-left) and ‘Profits by plunder’ (bottom-right). More simply, let’s just call them examples of good business versus bad business.

Is good business too much to ask? Hardly. First off, it’s the way business was characteristically practised until recently, including during its (American) mid-twentieth-century heyday. Second, it asks business to forsake neither self-interest nor the pursuit of profit. It simply requires that business not pursue self-interest and profit in ways that harm others. How is that unreasonable? (And what argument would business make as to why it should be allowed to inflict harm on others?)

More importantly, win–win behaviour is in the best interest of business. Treating others the way we want to be treated is the only behaviour that really works. It’s the behaviour that creates trust and fosters relationship. These are the essential building blocks of sustainable business success – trust and relationship with customers, with employees, with suppliers and so on. In fact without trust and relationship, business grinds to a halt.

It’s not surprising, then, that the empirical evidence for golden-rule behaviour in business is compelling. In The Ultimate Question, first published in 2006, Fred Reichheld introduced the powerful new business metric Net Promoter Score (NPS). Superficially, NPS measures how well or poorly a company satisfies its customers. But according to Reichheld, what NPS really measures is golden-rule behaviour. In turn, Reichheld marshals compelling data demonstrating that companies with superior NPS scores have substantially higher rates of profitability and growth than their competitors.

Similarly, in her 2013 book The Good Jobs Strategy, Zeynep Ton, one of the foremost retail operations experts, makes a powerful empirical case that – even in the extremely price-sensitive arena of low-cost retail – the most successful companies are the ones that pay and treat their workers well. Specifically, she found that these ‘good jobs’ companies were anywhere from 50 to 300 per cent better than their competitors at bottom-line performance metrics such as inventory turns, sales per employee and sales per square foot.

Let’s complement this with some anecdotal evidence:

Isadore Sharp, founder and chairman of the Four Seasons hotel group: ‘Our success all boils down to following the golden rule.’

Colleen Barrett, retired president of Southwest Airlines: ‘Practising the golden rule is integral to everything we do.’

Andy Taylor, CEO of Enterprise: ‘golden rule behaviour is the basis for loyalty. And loyalty is the key to profitable growth.’[22]

John Bogle, founder and former CEO, Vanguard Group: ‘You [only need] one rule … “Do unto others as you would have them do unto you.”‘[23]

The ‘golden rule’ is called that for a reason. Throughout human history it has been the gold standard for good behaviour. And for prudent behaviour. Profiting at the expense of others may work in the short term but not in the long. The merchant who delivers good value can expect to operate indefinitely; not so the knife-wielding mugger. Or as Jim Collins says in his seminal book Built to Last: ‘You can cheat your way to seeming greatness for five or ten years, but not for fifty or one hundred years.’[24]

It’s high time, therefore, for American public company CEOs to give up their profits-by-plunder myopia; high time to forsake win–lose value extraction and recommit to win–win value creation for all stakeholders. It’s how capitalism was always meant to work – for everyone.

[1] Edward L. Glaeser, ‘Can Business Do Well and Do Good?’, The New York Times, 6 January 2009; emphasis added.

[2] From Quote Investigator: Exploring the Origins of Quotations, http://quoteinvestigator.com/2011/02/23/capitalism-motives.

[3] From Quote Investigator: Exploring the Origins of Quotations, http://quoteinvestigator.com/2011/02/23/capitalism-motives.

[4] https://en.wikipedia.org/wiki/The_Virtue_of_Selfishness.

[5] Transcript of Milton Friedman interview quoted in ‘Donald Trump Says Greed Is Good’, by Aaron Sandler, The Daily Wire website.

[6] Which is not to say the divide between selflessness and self-interest is unimportant. It has considerable significance related to one’s character growth and spiritual development. But as regards outcomes, and the difference between right and wrong, moral and immoral, the dividing line of real consequence is between win–win mutuality and win–lose selfishness and predation.

[7] Mark Skousen, The Big Three in Economics: Adam Smith, Karl Marx, and John Maynard Keynes, Armonk, NY and London: M. E. Sharpe, 2007, p. 29.

[8] Mark Skousen, ‘Is Greed Good?’, Foundation for Economic Education, 1 May 2001; emphases in first paragraph added; emphasis in second paragraph original.

[9] Adam Smith, The Theory of Moral Sentiments, II.ii.2.

[10] In her excellent book The Shareholder Value Myth, the respected Cornell Law School professor Lynn Stout makes a convincing case that neither shareholders nor anyone else are the legal owners of corporations. That said, whatever their precise legal status, in the shareholder-centric version of business embraced in the USA since the 1980s, shareholders are clearly the effective and beneficial owners of public corporations – Lynn Stout, The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the Public, San Francisco, CA: Berrett-Koehler, 2012.

[11] Reprinted in Walther Ch. Zimmerli, Markus Holzinger and Klaus Richter (eds), Corporate Ethics and Corporate Governance, Heidelberg: Springer, 2010, pp. 173–8.

[12] Michael C. Jensen and William H. Meckling, ‘Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure’, Journal of Financial Economics 3:4, 1976, pp. 305–60.

[13] John F. Welch, ‘Growing Fast in a Slow Economy’, speech to financial community representatives, Hotel Pierre, New York, 8 December 1981.

[14] In fact it disadvantages long-term shareholders as well. A major study from the Harvard Business School, ‘Competitiveness at a Crossroads’, February 2013, comes to the blunt assessment that American business is losing the ability to compete in the global marketplace. Much of this is driven by companies’ squeezing research and development budgets to maximise short-term profits and fund dividend payments and stock buybacks.

[15] This chart comes from Andrew Smithers, economist and founder of Smithers & Co. Until recently he also wrote a recurring column for the Financial Times. The chart can be found at www.pbs.org/newshour/making-sense/merle-hazard. To be clear, SVM has not been the only driver of the disproportionate flow of business rewards towards owners and away from workers during the last few decades. Globalisation and automation have also had significant effect. Without the embrace of SVM, however, business would have looked for ways to mitigate the anti-worker effects of these other factors. Instead, SVM justified a wholesale embrace of any measures that fattened profits at the expense of workers and/or other stakeholders.

[16] ‘The Low-Wage Drag on Our Economy: Wal-Mart’s Low Wages and their Effect on Taxpayers and Economic Growth’, a report from the Democratic Staff of the US House Committee on Education and the Workforce, May 2013.

[17] Catherine Rampell, ‘Millennials Have a Higher Opinion of Socialism than of Capitalism’, The Washington Post, 5 February 2016.

[18] 2017 Edelman Trust Barometer: Global Annual Survey, 15 January 2017, www.edelman.com/trust2017.

[19] That said, it should be acknowledged that some businesses meet ‘needs’ that many may judge to be illegitimate – such as pornography or gambling.

[20] Nick Hanauer and Eric Beinhocker, ‘Capitalism Redefined’, Evonomics, 30 September 2015 – http://evonomics.com/redefining-capitalism-eric-beinhocker-nick-hanauer; originally published in Democracy: A Journal of Ideas, 31, Winter 2014 – http://democracyjournal.org/magazine/31/capitalism-redefined/?page=all.

[21] Developed by Eventide Asset Management, LLC as a guiding framework for ‘better investing for a better world’.

[22] All three quotations are from Fred Reichheld with Rob Markey, The Ultimate Question 2.0: How Net Promoter Companies Thrive in a Customer-Driven World, Boston, MA: Harvard Business School Publishing, 2011.

[23] John C. Bogle, ‘What I’ve Learned in a Half Century in Business – Twelve Rules For Building A Great Work Force’, 23 April 2003, www.vanguard.com/bogle_site/sp20030423.html.

[24] James C. Collins and Jerry I. Portas, Built to Last: Successful Habits of Visionary Companies, New York: HarperBusiness, 1994, p. xi.

An interesting example of market transformation can be seen in the growth of worldwide spending on beauty products, which reached $440bn in 2024. There are various trends (or pressures) at work, with men now feeling freer to spend on beauty products and demand growing among young people, who are purchasing such products at much earlier ages than their grandparents. Social media has played a significant role: as influencers share their beauty regimes, the online space is becoming the biggest shop window for the beauty industry. Additionally, there has been a shift in the marketing and consumption of beauty products, as consumers have become increasingly interested in the ingredients of the products that they buy and their supposed effects. In consequence, packaging is now plainer and bears something of the ‘laboratory look’.

Naturally there are concerns about trends among young people. With reports that beauty products are now being bought by children as young as eight, there has been alarm at the loss or increasing sexualisation of childhood, as well as concern about the damage that certain products can do to children’s skin. In consequence, there have been calls for regulation. It is normal to seek restriction or regulation of products that are deemed harmful, as witnessed in relation to tobacco, for instance, and more recently in connection with tobacco alternatives, such as of vapes and nicotine pouches. In connection with the beauty industry, one might wonder whether (or hope that) a ban on social media accounts for under-sixteens, as implemented in Australia and currently under consideration in the UK, will have an effect. Regulation in one sphere might affect associated behaviour in another. If young children are heavily invested in ‘beauty’ in an unprecedented manner – to the point of talking about anti-ageing products before they reach their teens – and social media influencers are in part responsible for driving such an interest, then restrictions on social media access could go some way towards addressing the problem. However, it is important to consider whether regulation is the answer.

The thought of the sociologist Max Weber (1864-1920) perhaps offers one means of shedding light on the issue. Weber described the phenomenon of ‘disenchantment’ and its effects on society. With the advance of reason and scientific principles, it becomes increasingly difficult to believe in spirits, gods or supernatural forces, with the result that the influence of religion and superstition is diminished. As the world becomes demystified and science is able to explain everything in rational terms, the world loses its mystery and appears mechanised and predictable. However, science cannot adequately fill the void created by the ousting of religion and people are no longer able to find the kind of meaning once provided by the values grounded in traditional beliefs; moral questions can be articulated and analysed, but not satisfactorily answered.

Some have questioned Weber’s account of the disenchantment of society, while others have proposed the possibility of re-enchantment: meaning and value – if they have indeed been lost – can be restored to the disenchanted world, either by projecting subjective values onto it, or by locating value as objectively existing in nature itself.

One interpretation of a shift in the market for beauty products might employ these concepts. Is the move towards a greater interest in the active ingredients of cosmetics a sign of an increasingly ‘scientific’ mindset, as society becomes more rational? Or is this in fact a form of re-enchantment, whereby ‘science’ – however ‘science’ is understood – is elevated to the status of religion and becomes a new dogma or article of faith? Do those who seek to buy plainly packaged cosmetics that resemble medicines display a tendency to deify ‘science’, almost to the point of seeking purpose and meaning in it? If influencers with questionable credentials in dermatology are helping to drive sales, perhaps such an account is not so far-fetched.

Perhaps the disenchantment thesis is able to make some sense of the disproportionate interest in beauty among young people, with children buying – or being given – adult cosmetics. In a disenchanted society in which transcendent values and traditional notions of meaning are lacking, preferences are shaped by other forces – or themselves become the locus of value and meaning. In either case, they can become disordered and unrestrained. Might skewed and superficial notions of beauty, driven in part by the forces of consumerism and assisted by social media, be behind the behaviour of some children? Where certain values have lost their influence, it is possible that people no longer see anything wrong with eleven-year-olds using anti-ageing products. If that is what they want and their parents have no objection, the thought might run, then so be it.

It is no surprise that there are calls to regulate access to social media for children. Social media – or its excessive use – has been associated with all manner of ills. The question is whether restriction will solve the problem. Likewise, we might ask whether, should the trend towards childhood use of adult cosmetics reach a scale at which it is felt that something must be done to protect the physical and developmental health of children, regulation would prove effective.

Markets simply match vendors with buyers, and it is something of a truism that businesses, if they want to survive, adapt to markets – or seek to shape them – in order to be able to offer a product for which demand exists. In the sense that the demand side of the ‘supply and demand relationship’ characteristic of markets is shaped by societal values, it is clear that markets do not simply serve society; they reflect it, too. When we hear calls for regulation to address problems, it is important to consider whether regulation can achieve the desired outcome. For instance, what manner of legislation could ever prevent parents from buying anti-ageing or beauty products for their barely-teenage children? In the absence of parental oversight, can any regulation really prevent determined teenagers from accessing social media? Parents who buy £1,000 phones and let their children scroll through social media until the small hours, or buy expensive, adult cosmetics for their children because ‘this is what she wants’ or ‘these are what her friends have’ are arguably not matters for regulation. These are questions of values.

Markets can only serve a society because to some degree, they act as a mirror of that society. Where markets are an expression of who we are or what we have become, concerns ought perhaps to be directed not at the statute book with a view to controlling the market itself, but at our own values: the attitudes of the society that the market both reflects and serves.

Image by Freepik (www.freepik.com)

Neil Jordan brings to CEME seventeen years’ experience of academic publishing, having previously served as a senior commissioning editor for Ashgate and Routledge where he specialised in research level publications in the social sciences. His primary focus was on sociology and social theory. Neil has also been employed as a teacher of philosophy and religious studies. He holds bachelor’s and doctoral degrees in philosophy, both from the University of Southampton, and has published on the subject of ethics.

Richard Turnbull

Capitalism is a complex word, even inadequate. Marxism uses the term in contrast to ‘labour’ (with the assumption that the accumulation of capital can only be at the expense of labour, a zero-sum game). Economic theory holds capital to be one of the ‘factors of production’, land, capital, labour and entrepreneurship, which at least allows for economic growth. Capitalism, at least in the public mind, may be linked with the opportunities, personal responsibility and individual freedom that lead to wealth creation, or with greed, lack of opportunity and inequalities that may lead to poverty – sometimes even in the same survey.[1] The Ipsos Mori Veracity Index 2016 lists ‘bankers’ and ‘business leaders’ in 19th and 20th places out of 24 professions in terms of being ‘trusted to tell the truth’.[2]

There are many dilemmas. The globalisation of world trade has extended the benefits of growth, not least reductions in global poverty, but not only is the growth shared unevenly, the exclusion of many from the benefits leads to alienation. Corporate structures have tended to reinforce rather than resolve the problem. Oligopolistic markets that lack real competition are not really capitalism at all. Neither are public bailouts for failed businesses – even banks; more like socialism for the already wealthy. Corporate values and ethics as expressed in a firm’s statement of purpose, mission or values have not prevented scandal.

So for some, the recovery of moral purpose in capitalism is an oxymoron. Nevertheless, the fact remains that it is the capitalist economic system that, for all its failings, delivers goods and services, well-being of individuals and communities, provides employment and opportunity and encourages enterprise and entrepreneurship. The recovery of moral purpose for capitalism, rather than being a contradiction, is the essential prerequisite for its effectiveness.

Therefore perhaps capitalism is the wrong word to describe an enterprise, market-based economy built on values of purpose, service and integrity. In other words, an economy with values shaped historically by the Judaeo-Christian ethic, encompassing growth, reward, incentive and opportunity, but also fairness, responsibility and compassion as integral elements. Yet capitalism is here to stay. Adjectives such as inclusive, conscious, restorative, relational have all failed to capture the imagination. What capitalism needs is not a new definition but the restoration of moral purpose in markets, in business purpose, conduct and structure and, indeed, in the character of market participants.

However, we should begin by setting out the contours of capitalism or enterprise. The debate too often begins in the wrong place – a rogue trader in a bank, a corporate scandal or issues of executive pay. From the problems, solutions are debated. The issues may indeed be very important, but if there is to be a holistic approach to creating an enterprise economy, then it is essential to begin with a vision for the market economy itself.

At the heart of the moral case for enterprise and capitalism is, first, the necessity of wealth creation for the economic and moral well-being of society. The most effective mechanism for achieving the economic growth necessary for the common good is the market economy. This is the means for the provision of goods and services, the management of savings and investment, the encouragement of the propensity to save, the provision of employment and a tax base. The market economy brings inestimable benefits to society. As the late Michael Novak (1933–2017) notes:

Of all the systems of political economy which have shaped our history, none has so revolutionized ordinary expectations of human life – lengthened the life span, made the elimination of poverty and famine thinkable, enlarged the range of human choice – as democratic capitalism.[3]

This, he argues, means ‘a predominantly market economy; a polity respectful of the rights of the individual to life, liberty and the pursuit of happiness; and a system of cultural institutions moved by ideals of liberty and justice for all’.[4] The evidence for the positive impact of the market on poverty reduction is insurmountable. Extreme poverty has fallen.[5]

A second crucial element to capitalism is freedom to trade and undertake economic activity. The market brings buyer and seller together, who trade, to mutual advantage, at the agreed price. William Bernstein tells the extraordinary story and history of trade and the overwhelming mutual benefit humanity has gained from the principle of trade: ‘World trade has yielded not only a bounty of material goods, but also of intellectual and cultural capital.’[6]

Both these points, which are all too frequently lost in debate, are reinforced by Milton Friedman’s observation that he knew of ‘no example in time or place of a society that has been marked by a large measure of political freedom, and that has not also used something comparable to a free market to organise the bulk of economic activity’.[7]

Economic growth, of course, is a contested area. For some, ‘only relative growth is possible: the global economy is playing a zero-sum game, with an ever-shrinking pot to be divided among the winners.’[8] However, without the wealth creation generated by the market, which leads to economic growth, it is impossible to deal effectively with issues of poverty and social welfare; to suggest otherwise is illusory.[9] Indeed, ‘higher per capita income is strongly correlated with some undeniably important factors, such as longer life expectancy, lower incidence of disease, higher literacy and a healthier environment.’[10]

Third, the propensity to save. The importance of savings – deposits, investment funds, life and pension funds – is often overlooked. The efficient pooling and investment of this capital in high-quality, innovative companies, technological advance and product development is an essential driver of growth and employment in an enterprise economy.

The market is an efficient mechanism but it is not perfect. There are problems of monopoly, oligopoly, price fixing and the fact that the market is populated by individuals who are themselves not perfect but flawed. In the same way that the benefits of the market cannot be ignored, neither can its imperfections. Similarly, economic growth may accrue unevenly. Thus the market may lead to inequalities. Equality is not a goal per se – but extreme inequalities reinforce the loss of opportunity in an economy, significantly dampen aspiration and may result in lack of access to justice or the other basic institutions of civil society.

The first problem lies then in the failure of competitive markets. So, for example, in both banking and energy sectors in the UK, the market is dominated by a small number of large players. The consequence of this is that price competition is reduced, consumer choice may be limited and there are significant barriers to entry and the potential for restrictive practices. Reduced choice and high prices disproportionately affect the poor. In the early 1800s there were some 800 country banks, outside London. With the advent of joint-stock companies there were, by 1866, some 154 joint-stock banks that were members of the clearing house system; now there are just five.[11]

The second problem is the painful consequences of reallocating capital. The impact of the movement of capital from a dying or declining industry into new areas of growth has significant and negative structural impact. This may be true in terms of unemployment, the knock-on effect on consumer spending, issues of poverty and structural decline of communities. The market may indeed bring about long-term recovery but the impact of the decline and its effects cannot be denied. For example, in 1971 there were, in the UK, 320,000 people employed in the steel industry. By 2015 this had fallen to 21,000 (with a further 10,000 in steel processing). From 1975 to 2015, employment in the steel industry in Wales fell from over 60,000 to 8,500.[12] The brunt of this impact has fallen on particular communities, such as, for example, Port Talbot in South Wales.[13]

The third issue is the exploitation of power often seen in examples of corporate and personal greed. This perception of corporate greed is further reinforced by apparent rewards for failure, excessive remuneration and failings in corporate governance. All of these things underline the sense of ‘crony capitalism’, the accumulation of capital by the few, and greed.[14]

The point is that a combination of capital accumulation, globalisation of production, structural decline in industries and failings of corporate governance, combined with greed and malpractice, produces effects that cannot be ignored.

The market economy has always attracted people of faith. The reasons are, of course, varied. Sociologists will point to the ‘Protestant work ethic’ and the formation of what Max Weber referred to as ‘the spirit of capitalism’.[15] In other words, Protestants worked hard for the Lord in the world, their faith of individual discipline shaping a work ethic. For others, such as the Quakers, persecution and exclusion from the universities and from public office meant that many turned not only to business per se but also to technological research and development. Quaker involvement in manufacturing and banking went considerably beyond their numerical influence. It is quite extraordinary how many of our companies – Cadbury, Barclays, Huntley & Palmer, Clarks – had Quaker origins. The Quakers produced ‘advices on trade’ over many decades, warning against everything from overtrading to indebtedness and advocating the priority of good accounting. They made provision for the welfare of their employees – from sick pay to pensions; from savings banks to model housing.[16]

However, these explanations are only partial. Two other factors have formed and shaped how people of faith have influenced business. First, the development of culture. People of faith have often formed networks of families, contacts, even schools and so on. These factors led to a culture of trust and integrity in business dealings. Trade networks, credit finance, apprenticeships all developed through these culturally shaped groupings. In addition to that, most religiously minded people had clearly developed moral codes – for the Christian most usually the Bible – and as a consequence, habits of moral behaviour (honesty) also translated into business practice: fair pricing, resistance to bribes, weights and measures and indeed concern for employees and wider society.

Faith provided, for some though not all, a framework of culture and conduct. Both of those aspects of a moral, purposeful, inclusive business ethic are today often sadly lacking.

In 1987 one of the leading chemical conglomerates at the time, ICI, described its purpose as follows:

ICI aims to be the world’s leading chemical company serving customers internationally through the innovative and responsible application of chemistry and related science. Through the achievement of our aim we will enhance the wealth and well-being of shareholders, employees, customers, and communities which we serve and in which we operate.

In 1994 the company objective had changed to:

Our objective is to maximise value for our shareholders by focusing on businesses where we have market leadership, a technological edge, and a world competitive cost base.[17]

So what changed? What changed so that ICI no longer aimed to be ‘the world’s leading chemical company’? What changed such that ICI’s application of science was no longer to be ‘the innovative and responsible application of chemistry and related science’ but only that in which they had ‘a technological edge’? What happened to the ’employees, customers, and communities which we serve’, to be replaced by ‘to maximise value for our shareholders’?

The case of ICI is illustrative of the way business has become separated from ethics, values and a truly holistic purpose that serves the economy and society well.[18]

The problem lies in the way ‘shareholder value maximisation’ has become the single measure of business return. Continued adherence to this mantra imperils the future of the enterprise economy.

Profit – the surplus of revenues over costs, the value added to goods in the process of manufacture and sale – is a deeply moral concept. Profit is essential to the proper, effective and long-term functioning of a business. However, profit is essentially a by-product of purpose.

The objective of profit does not stand alone but is set in the context of a business’s wider purposes. It is one that brings value to our ever globalised, ever competitive marketplace, in a manner that continually strives for a goal that is greater than itself. Profit becomes a by-product of this purpose-driven business model.[19]

Shareholder value maximisation is one of several factors that encourage short-term decision-making over long-term values. Others would include the tenure of CEOs, the expectations of quarterly reporting and executive remuneration based on short-term performance. Current shareholders benefit at the expense of future shareholders. The conclusion might be that all that matters is the current share price and hence company valuation. Not so.

Bill Drayton, founder and chairman of Ashoka: Innovators for the Public, and named in 2005 as one of the 25 best leaders in the USA by US News and World Report, observes: ‘For three centuries the social and business halves of society drifted apart. So far apart that they developed different languages, styles, legal structures, and mutually negative stereotypes of one another.’[20] This separation goes to the heart of why business has become compartmentalised from the communities and societies whose fundamental consent and licence is essential for enterprise to operate effectively. The social contract is breaking down.

This separation is not one that can be simply bridged by corporate social responsibility, which is more a symptom of the divide than a solution.

Historically the business world has been more connected to communities and society in both direct and indirect ways. In the nineteenth century many factory owners developed ‘model villages’.[21] The idea that industrialists, entrepreneurs and business owners might build such model villages is, to many, surprising if not somewhat baffling. These villages remain today as monuments to a bygone age. However, their development reminds us that in the period of the great Quaker firms, business magnates had a real vision for the relationship of business, family, workforce, locality and wider society.

The model villages were an expression of this integrated vision. In Bournville the houses had gardens; there was planned open space, a village green, cricket ground; and provision was made for schools, worship, shops, adult education facilities, libraries, schools, baths and so on. Both Cadbury and Rowntree decided against ‘out and out sale of housing at cost price’[22] or anything that had the ‘stamp of charity’,[23] preferring long leases with mortgages and deposits on a sliding scale.

There were wider housing examples in London. The Artizans’, Labourers’ and General Dwellings Company, a for-profit joint stock company whose President was the Christian social reformer Lord Shaftesbury, built 6,400 residences for working people by 1900, accommodating 42,000 people. Other examples included the Four Per Cent Industrial Dwellings Company – the clue being in the name – and the Metropolitan Association for Improving the Dwellings of the Industrious Classes, which adopted business principles for social purposes. Business principles and capital return for social good.

The nineteenth century also saw the beginnings of micro-finance and local banking. The Emily Loan Funds were established in memory of Lord Shaftesbury’s wife, who died in 1872. They were aimed especially at flower sellers who could not operate in winter. The Fund would loan an amount to enable these women to purchase stocks of goods suitable for sale in winter or else the hire of a potato oven. Other similar ‘finance societies’ funded the purchase of barrows or donkeys with low-cost loans. We also see banking at work among the poor, pertinent today in our debates about credit unions and so on. Penny Banks and Provident Societies were effectively savings banks, taking small deposits on a weekly basis.

Today this application of business skills to social problems is called ‘social entrepreneurship’ and ‘social impact investing’. The Organisation for Economic Co-operation and Development (OECD) defines social impact investment as investment made ‘with the intention of generating a measurable, beneficial social and environmental impact alongside a financial return’.[24] There are other ways of approaching the issue of definition but the essence is that social impact investing involves both financial returns and measurable social impact.

Social enterprises have become one of the new modes of business organisation for social purposes. The most effective social enterprises use a variety of means of capital, including venture capital and private equity. In addition, there will be robust governance structures, highly skilled individuals, diverse partners and a clarity of social vision. In this way it is possible to harness significant funds to achieve social purposes through the application of business skill and commercial objectives.

How then are we to respond to these changing features of capitalism and restore moral purpose to the heart of an enterprise economy?

Purpose needs to be restored to business. This restoration of purpose cannot be reduced to either legislative or corporate social responsibility. However, as a starting point, the repeal of section 172 of the Companies Act 2006 would signal intent. Section 172 requires directors to act for the success of the company for the benefit of members (effectively shareholder value maximisation), while having regard for employees, customers, suppliers and environmental impact. The effect of the section is to establish a hierarchy of priorities. As Professor Andrew Keay has said, the bottom line is: ‘Did the action promote the success of the company for the benefit of the members?’[25]

However, purpose cannot simply be legislated for. Purpose and values can only be implemented in a culture. Both the history and academic study tells us, as Professor Mark Casson has argued, that ‘the quality of entrepreneurship depends on the quality of business culture.’[26] So one further step is to emphasise that business success cannot be measured by a single numerical value. A second step is to think about how culture is determined. There may, in this regard, be considerable differences between the culture of a small- or medium-sized enterprise (SMEs) and that of a large corporate entity. A small, family-run company is likely to have a very strong culture, which may be benevolent or otherwise; a large corporate may have more defined processes and perhaps a very open culture, but face significant pressures on culture from middle management in particular.

A business culture can be defined as the attitudes, expectations and processes that shape the behaviour of a company and its employees in the conduct of business. Culture therefore includes both formal and informal aspects, personal characteristics and example, as well as good-quality processes. The key challenge is how to implement these expectations throughout a company.

The complexity is this: to argue that, for example, a culture should be transparent is easy to write but less so to implement. However, there are some questions that might help in forming and shaping an appropriate corporate culture:

The idea of the joint-stock company – that is, a company with external shareholders who share fully in the profits but are limited in their losses – has been a vehicle for raising capital for investment for over 150 years. While the structure has many advantages, its ambiguity is shown by the simple fact that prior to 1855 (the introduction of the Limited Liability Act), the establishment of a joint-stock company required an Act of Parliament. Even The Economist recognised the complexity: in 1856 the magazine regarded limited liability as overrated; by 1929 as indispensable.[27]

The answers to the problems of capitalism do not in themselves depend on corporate structure. However, structure can provide a framework from which other matters flow. Indeed, society is increasingly recognising the importance of corporate governance.

There are two aspects to consider. The first is formal structure. There are those, such as the B Corporation movement, who advocate formal changes to corporate structure, such as through the Memorandum and Articles of Association and an accreditation process. Professor Colin Mayer advocates a ‘trust company’ with a ‘board of trustees’ responsible for the stewardship of corporate values and voting rights dependent on the length of time equity shares are held.[28] More detailed reflection on the relative merits of such approaches is beyond the scope of this chapter. However, in essence the more company law allows for a wider and greater variety of structures, the greater the opportunities for exploring new ways of inculcating purpose and values within a corporate structure.

The second aspect is new approaches within the current structures. The idea of the non-executive director is a powerful one in terms of checks and balances within the system. The problem is that many non-executives fail to maintain the vigorous independence the role requires. Similarly, for some the non-executive role becomes a career in itself. Thus the professions and the professional bodies should be encouraged to widen the pool of potential non-executive directors through identification, mentoring and training. Similarly, some consideration should be given to restricting the number of non-executive roles that may be held by one individual simultaneously, so that full attention can be given to the discharge of the responsibilities.

There is also the question of the handling of certain ‘hot potato’ topics. Executive remuneration is probably the most significant of these but there may also be supply-chain, environmental or employee-related issues. In essence these are reputational matters. A healthy capitalism does not mean that executives should not be well remunerated or that credit should not be taken from suppliers. However, companies with good ethics and values will want to ensure that pay reflects merit and long-term performance; that smaller suppliers are not exploited in respect of payment terms; that the contractual arrangements of employees are not abnormal, unreasonable or exploitative; and that firms take seriously their environmental impacts. In essence, clear and transparent policies are the key here, although some would argue, for example, that a company’s annual remuneration report (if applicable) should be formally voted on by shareholders or the ratio of pay within the company published. These suggestions may indeed warrant adoption, but a more radical approach would be for an annual report from the independent non-executive directors covering all the key areas of risk or contention, such a report requiring to be approved at the AGM, published on the website and circulated to all employees, key customers and suppliers.

We are, in our current age of diversity and tolerance, very wary of enjoining moral codes on others. Ultimately the question is one of character. No amount of legislation, structural organisation or regulation can force good behaviour. However, society needs, for the good of business, the economy and civil society to draw a distinction between the moral and moralising. The former is a state of mind, an attitude of heart, a recognition of responsibility and an appreciation of the impact of values on behaviour. The latter is more of the nature of ‘injunctions’ concerning particular behaviours. The consequences of a failure to appreciate the central importance of moral character was clearly espoused by a quote, which although unsourced, is famously attributed to Theodore Roosevelt: ‘To educate a person in the mind but not in morals is to educate a menace to society.’

Among the consequences of moral character are a responsible attitude to wealth and also to society. The steely discipline that shapes an entrepreneur – the patient wait for return – is likely to enhance a view of wealth that recognises that such wealth was hard earned, is transient and carries responsibility. Equally, the apparent rugged individualism of the entrepreneur usually belies the reality of a team and a culture. Values shaped in such a setting are more likely to recognise a wider responsibility to civil society – or as was illustrated in the original corporate objectives of ICI: ‘to serve … the communities in which we are set’. Just like Cadbury at Bournville.

The future of capitalism, its nature, shape and organisational features, is essential to a healthy society and indeed an inclusive economy. Capitalism carries innumerable advantages for everyone. However, all is not well. This is partly due to structural problems within the market economy but much more so because capitalism as practised today has, regrettably, rather lost its way. A breadth of purpose, responsibility towards wealth, recognition of the impact on our communities and civil society, and above all the restoration of moral character and discipline, would go a long way towards repairing the tear. We need not call this ‘moral capitalism’ or ‘inclusive capitalism’; better just ‘capitalism’. Yet the word is problematic. An ‘enterprise economy’ sounds so much better.

[1] Public Religion Research Institute, Economic Values Survey 2013.

[2] Ipsos Mori Veracity Index 2016, www.ipsos-mori.com/researchpublications/publications/1896/Enough-of-Experts-Ipsos-MORI-Veracity-Index-2016.aspx.

[3] Michael Novak, The Spirit of Democratic Capitalism, Lanham, MD: Madison Books, 1982, 1991, p. 13.

[4] Novak, Spirit of Democratic Capitalism, p. 14.

[5] United Nations, The Millennium Development Goals Report 2015, New York: United Nations, 2015.

[6] William J. Bernstein, A Splendid Exchange: How Trade Shaped the World, London: Atlantic Books, 2009, p. 384.

[7] Milton Friedman, Capitalism and Freedom (40th anniversary edn), Chicago: University of Chicago Press, 2002, p. 9.

[8] Richard Heinberg, The End of Growth: Adapting to Our New Economic Reality, Gabriola, BC, Canada: New Society Publishers, 2011, p. 2; emphasis in original.

[9] Daniel Pinto, Capital Wars, London: Bloomsbury, 2014, ch. 2.

[10] Wayne Grudem and Barry Asmus, The Poverty of Nations: A Sustainable Solution, Wheaton, IL: Crossway, 2013, p. 47.

[11] A Report on the Culture of British Retail Banking, Cass Business School/New City Agenda, November 2014. See also British Banking History Society, www.banking-history.co.uk/history.html.

[12] House of Commons Library Briefing Paper, October 2016, ‘UK Steel Industry: Statistics and Policy’, p. 6.

[13] National Assembly for Wales, Research Briefing, ‘The Steel Industry: An In-depth Look’, May 2016.

[14] Examples include the original ‘rogue trader’, Nick Leeson, who brought down Barings in 1995, the recent accounting scandal around overstated profits at Tesco in 2014 and the controversy over Philip Green’s sale of BHS and its pension fund deficit in 2015.

[15] Max Weber, The Protestant Ethic and the Spirit of Capitalism, first published in German in 1905. Multiple modern translations and editions are available.

[16] For a full analysis see Richard Turnbull, Quaker Capitalism, Oxford: Centre for Enterprise, Markets and Ethics, 2014.

[17] www.theguardian.com/business/2007/jun/24/manufacturing.observerbusiness.

[18] See analysis by John Kay, Obliquity: Why our Goals are Best Achieved Indirectly, London: Profile Books, 2011.

[19] Andrei Rogobete, Ethics in Global Business: Building Moral Capitalism, Oxford: Centre for Enterprise, Markets and Ethics, 2016.

[20] Bill Drayton, ‘The Citizen Sector Transformed’, in Alex Nicholls (ed.), Social Entrepreneurship: New Models of Sustainable Social Change, Oxford: Oxford University Press, 2006, p. 51.

[21] Examples include Bournville, Saltaire, New Earswick, Port Sunlight.

[22] P. Henslowe, Ninety Years On: An Account of the Bournville Village Trust, Birmingham: Bournville Village Trust, 1984, p. 3.

[23] Joseph Rowntree Village Trust, One Man’s Vision: The Story of the Joseph Rowntree Village Trust, London: Allen & Unwin, 1954, p. 4.

[24] OECD, ‘Social Impact Investment: Building the Evidence Base’, Paris: OECD, 2015, pp. 58–9.

[25] Professor Andrew Keay, presentation at Guildhall Chambers on ‘Promotion of the Success of the Company – Section 172’.

[26] Quoted in A. Prior and M. Kirby, ‘The Society of Friends and Business Culture 1700–1830’, in D. J. Jeremy (ed.), Religion, Business and Wealth in Modern Britain, London and New York: Routledge, 1998, p. 115.

[27] Quoted in B. C. Hunt, The Development of the Business Corporation in England 1800–1867, Cambridge, MA: Harvard University Press, 1936, p. 116.

[28] Colin Mayer, Firm Commitment: Why the Corporation is Failing us and How to Restore Trust in it, Oxford: Oxford University Press, 2013.

Chris Pinney

Few would disagree that capitalism is the most powerful economic system humanity has developed. Capitalist societies have experienced unprecedented economic and social progress, creating the highest standard of living the world has ever seen. It is the principles behind capitalism, such as individual rights, private property and free markets that generated the entrepreneurship, technological innovation and wealth that gave rise to the middle class in the seventeenth century. This in turn drove the political movements that overthrew monarchies and autocrats, leading to the development of the modern democratic state and the many freedoms its citizens now enjoy.

At the same time, it was the rise of nineteenth-century industrial capitalism and the impact on workers and income inequality that created a populist backlash against capitalism in the early twentieth century, giving rise to socialist movements and communism. As we enter the twenty-first century, it is a global capitalist economy that is once again seen as driving income inequality and disenfranchising workers in developed economies while exploiting those in emerging markets. As at the turn of the last century, we once again see a strong populist backlash against global capitalism and a growing political turmoil and uncertainty. In How Will Capitalism End? the economist Wolfgang Streeck notes that capitalism for the foreseeable future will hang in limbo, dead or about to die from an overdose of itself. Streeck envisages a ‘society devoid of reasonably coherent and minimally stable institutions and a period of uncertainty and insecurity’.[1]

Despite these sorts of gloomy predictions, there is good reason to believe that capitalism can be re-imagined to avoid a rerun of the early twentieth century. To do so will require a fundamental rethink of the failing social contract that successfully balanced the interests of markets with the broader interests of society for the last 60 years. We now need to re-examine the responsibilities of the private, public and civil society sectors in managing a global capitalist system. We should question what each must now do to ensure capitalism continues to play its vital role as an engine for economic and social progress. Finally, we must also examine the values and principles required to ensure that markets work effectively and fairly.

This chapter offers some thoughts on these themes from three perspectives. The first considers how the technological innovations driven by capitalism reshape society and its political and social institutions. The second considers the values, principles and assumptions that gave rise to capitalism and how they can inform the future. The third explores the unravelling social contract that has governed capitalism for the last 60 years and how it can be restructured to support twenty-first-century capitalism.

Over the last 500 years, capitalists in search of new ways to produce products more efficiently and profitably have been the driving force behind successive waves of technological innovations that transformed the economy from an agricultural to a mercantile one, from an industrial to a now globally integrated ‘post-industrial’ society. Each wave of innovation has dramatically lifted productivity, driving economic growth and increasing the returns to capital and to labour. While each advance has destroyed jobs in the previous economy, they have at the same time generated new jobs and income for workers as capitalists and their companies created new categories of products and services that raised the standard of living for all. For example, real per capita GDP in the USA grew nearly sevenfold during the twentieth century, and despite fluctuating levels of income inequality, standards of living improved for all economic groups, including the bottom 20 per cent of income earners. In 1900, fewer than one in five homes in the USA had running water, flush toilets, a vacuum cleaner or gas or electric heat. In 1950, fewer than 20 per cent of homes had air conditioning, a dishwasher or a microwave oven. Today, 80–100 per cent of American homes have these modern conveniences. As for standards of health:

Average life expectancy in the U.S. has grown by more than 50 per cent since 1900. Infant mortality declined from 1 in 10 back then to 1 in 150 today. Children under 15 are at least 10 times less likely to die, as one in four did during the 19th century, with their death rate reduced by 95 per cent.[2]

As we enter the twenty-first century, capitalism is driving the next wave of technological innovation, namely machine intelligence. This new wave of technology, coupled with the impact of the globalisation of the world economy, has profound implications for our economic model and society. On the one hand, this innovation has the potential to continue to improve quality of life and dramatically reduce the need for human labour in dangerous industrial jobs or boring and repetitive tasks in service industries. On the other hand, it raises fundamental questions about the future of work and the way income is distributed in society. This leads to far-reaching implications for our economic model and the political and social institutions that govern capitalism.

According to David Autor, an MIT economist who has studied the loss of middle-class jobs to technology, ‘it will be harder and harder to find things that people have a comparative advantage in versus machines’, a point reinforced in a blog called Welcome, Robot Overlords: Please Don’t Fire Us?[3] Indeed, half of the 7.5 million jobs lost during the ‘Great Recession’ were in industries that pay middle-class wages, which are defined as ranging from $38,000 to $68,000. Since the official end of the recession in June 2009, only about 70,000 – or 2 per cent – of the 3.5 million jobs gained have been in such mid-paying industries. At the same time, nearly 70 per cent of the restored jobs have been in low-paying industries. In the 17 European countries that use the euro as their currency, the numbers are even worse. Almost 4.3 million low-paying jobs have been gained since mid-2009, but the loss of mid-paying jobs has never stopped. Indeed, a total of 7.6 million such jobs are said to have disappeared between January 2008 and June 2013.

As more of the wealth generated by globalisation and machine intelligence goes to capital and large firms, so their influence on political systems increases. As the MIT economist Daron Acemoglu and James Robinson, a Harvard political scientist point out, although free markets tend to create widespread prosperity, they also have the potential to create concentrations of wealth and political power that are often used to suppress competition and entrench rent-seeking elites. This in turn further slows economic growth and income to labour. This skewed distribution of wealth has contributed to rising inequality, the decline of the middle class and the growth of a working poor ‘underclass’ whose inadequate education and low skills leave them with poor prospects for full participation in the economy as wage earners or consumers.

Some economists, including Thomas Piketty in his bestselling book Capital in the Twenty-First Century,[4] have argued that the period of high economic growth and moderate levels of income inequality in the developed economies during the last century are in fact an anomaly compared to historical norms. Piketty attributes the low levels of income inequality during this period to social upheavals, economic depressions and wars that shook up the social order, destroyed wealth and returns to capital and gave rise to pressures for higher taxation on both high-income earners and inherited wealth. But Piketty suggests that during the last 50 years, a period of relative stability and rising incomes in the developed economies, these pressures have moderated, contributing to a steady decline in tax rates on the wealthy. Therefore he postulates that we may now be returning to a norm in which the private return to capital exceeds the rate of national income and output. This condition, in the absence of high levels of taxation, is expected to accelerate the flow of income to those with capital and away from labour, leading to ever greater inequality and potential political unrest.

Piketty’s analysis is clearly reinforced by recent data. Until a decade ago, the share of total US national income going to workers was relatively stable at around 70 per cent. The share going to capital – mainly corporate profits and returns on financial investments – made up the other 30 per cent. Slowly but steadily, however, labour’s share of total national income in the USA and other OECD countries has been falling, while the share going to capital owners has gone up. During the period 2010–12, the top 1 per cent are said to have received 95 per cent of the growth in income and, according to a 2013 Credit Suisse report, now own 41 per cent of all global assets.

It is not surprising given these trends that capitalism finds itself in crisis. Once again, those who feel behind or maltreated by global capitalism are rallying behind populist and socialist movements seeking to challenge rising inequality and the power of capital over the economy and society. As in previous transitions, there is a heated debate about the values, principles and assumptions that underlie capitalism and the social contract that supports it.

Central to capitalism’s future success will be the need for a set of principles that can balance the self-interest of market participants with the broader interests of society. As we consider the road ahead, it will be useful to reflect on the values that have driven capitalism’s success in the past and how they can be drawn on to shape the path forward.

The foundations of capitalism were laid at a time when Catholicism still predominated and daily work itself was considered profane and mundane. It was the early Protestants Martin Luther (1483–1546) and John Calvin (1509–64) whose writings first established the perspective that daily work and self-improvement was a legitimate way to be in service of God’s will and therefore encouraged. It was Calvin’s writings around asceticism – frugality, rational planning and delayed gratification in service of God – that formed the backbone for the Protestant work ethic that in turn provided a strong underpinning for an emerging capitalist society.