Ethical Machines by Reid Blackman is one of the more recent books published that seek to make sense of the intersection between the domain of artificial intelligence, machine learning and the moral questions associated with the use of these technologies. This being all applied within the context of a company and its use of AI.

Reid Blackman is currently the CEO and founder of Virtue, an ethics AI consultancy that specialises in ethical risk mitigation and the implementation of artificial intelligence. Prior to this, Blackman was a professor of philosophy at Colgate University and the University of North Carolina, Chapel Hill.

Contrary to what the cover would suggest, Ethical Machines is more concerned with dispelling the myths surrounding the field of ethics rather than a technical discussion on AI itself. This perhaps comes as no surprise since the author’s background is primarily in philosophy, not computer science.

The book is comprised of seven chapters. Blackman makes extensive use of the first person and writes in an informal tone, making the book sometimes read more like personal diary than a specialised piece of literature (which paradoxically it is). No doubt readers will have their own personal preference so this might not necessarily be a negative feature.

Unlike most of the other books reviewed on this website, Ethical Machines is not aimed at the general public or even the inquisitive reader, but rather the business community and in particular, business leaders and managers that are trying to get their heads around implementing ethics in their firm’s use of AI.

The premise of the book seeks to dispel the myth and scepticism surrounding ethics as a subject and as something that can be defined and even implemented in quantifiable way. Blackman’s argument is that managers and those in decision-making positions are struggling to implement ethics because they are trying to “…build Structure around something they still find squishy, fuzzy, and subjective. They’re doing a lot of AI risk mitigation, and while they may know a lot about AI and risk mitigation, they don’t know much about ethics” (page 14).

The book’s thesis therefore is that an organisation can never achieve a “comprehensive and robust Structure” if it fails to understand ethics – i.e. the “Content side of things” (Ibid). In this case “Structure” refers to a governance structure: the “policies, processes, role-specific responsibilities […] a set of mechanisms in place to identify and mitigate the ethical risks it may realise in the development, procurement, and deployment of AI” (page 16). “Content” on the other hand refers to the ethical risks that the company wants to avoid (Ibid).

Chapter I opens the discussion by making an attempt to transform the general preconception of ethics as something that is “squishy” or “subjective” to something that is concrete (page 23-24). Blackwell argues that in order to better understand ethics one must first ask a series of questions that most people would consider to be ethical, such as: “What is a good life?”, “Do people have equal moral worth?”, “Is it ever ethically permissible to lie?”, and so on (page 26).

Chapters II – IV deal primarily with three larger problems surrounding the field of AI. The first is the issue of bias in AI and the challenges that data interpretation brings. The second is known as “explainability” (page 61) that looks at the journey between the input data and the resulting output data. The third and final issue is the problem of privacy in the use of AI and more importantly, the interplay between AI, privacy, and ethics (page 87).

Chapters V – VII are more focused on the structure side of things in implementing an AI ethical risk programme. Chapter V looks at how to construct an AI ethics statement that ideally changes behaviour and is not another PR experiment. Chapter VI further develops upon this and looks at what an effective structure or AI ethical risk programme actually looks like within the firm. The author emphasises that “…there is no such thing as a viable and robust AI ethical risk program without leadership and ownership from the top” (page 162). Chapter VII ends the discussion by specifically paying attention to the development team and their approach to implementing AI ethics in the product creation process. Blackman argues that rather than applying any particular moral theory, developers should instead focus on the wrongs – “the avoidance of harming people” (page 185).

In concluding, Ethical Machines is a curious addition to the literature on AI ethics. No doubt that there will be eyebrows raised amongst some readers, particularly those with a background in business who might be less convinced by the feasibility of Blackman’s approach. Some may doubt that trying to discover what is morally wrong will help clarify a firm’s ethical stance. This is particularly problematic when there are likely to be disagreements within the firm about the exact position of the ethical barometer with regards to any given issue.

Nonetheless the book offers plenty of food for thought – those with an interest in how AI ethics can be better understood and applied within the context of a firm will likely find it a worthwhile endeavour. However, those looking for a discussion on AI itself will best be served elsewhere.

Ethical Machines: Your Concise Guide to Totally Unbiased, Transparent, and Respectful AI by Reid Blackman was first published in 2022 by Harvard Business Review Press (ISBN. 1647822815, 9781647822811), 224pp.

Andrei E. Rogobete is the Associate Director of the Centre for Enterprise, Markets & Ethics. For more information about Andrei please click here.

In my last blog post from the early days of the leadership contest I stressed the need for the next prime minster to care about economic growth. We now do, but will this be sufficient?

The growth rate of the UK after the financial crisis has hurt families and the public coffers relative to an alternative where the growth rate was higher. If the economy had kept growing at the level before the crisis, the average household would make thousands of pounds more per year and be more able to weather crises. The UK would be wealthier and more capable of borrowing and servicing debt.

The government is changing many policies including some which economists across the political spectrum have argued for. For instance, stamp duty and corporate taxes raise revenue in ways that reduce the performance of the economy. The first being a transaction tax that prevents the efficient allocation of housing, and the latter discourages investment especially without the introduction of full capital expensing. The critiques of these were well outlined by Tom Clougherty of the Centre for Policy Studies ahead of the announcement. The best bullish supply-sider reaction to the policies came from Ryan Bourne.

These reforms are growth-enhancing but are taking place at a time where the fiscal demands of the UK are rising primarily due to a) unfunded increases in spending from policies passed by the government in response to the energy crisis b) the rise in increase rates and c) reduced direct revenue from taxes. At least some of the reductions in revenue will be made up in the future by taxes from the resultant economic growth, but as many have argued, this course of action is a gamble. The widespread depiction of the language suggests that the fiscal gamble is the result of the more controversial policies (bankers’ bonuses, additional rate, etc) while much of the gamble is the result of pre-existing policies.

The biggest fiscal impacts (see Table 4.2) of the new government have been the widely supported residential and commercial energy policies and the reversal of new tax increases (raising the corporate tax rate to 25% while phasing out capital expensing brought in by Chancellor Sunak and introducing a National Insurance levy). The National Insurance hike similarly been criticised by many for raising taxes on all workers (both directly and through their employers) during the cost-of-living crisis.

Insofar as these policies are representative of the direction of travel in Westminster, onlookers should be less frightened this week than they were before the announcements. There is scope for growth-enhancing reforms with little direct fiscal cost (something I will discuss in a follow up blog post). The fact that the chancellor and prime minister put forward these policies is a sign that unlike their predecessors they are both primarily interested in economic growth and willing to use political capital to pursue it. The growth plan issued by the Chancellor to detail the changes adopts a 2.5% growth target and claims that “economic growth is the government’s central mission.”

The other reforms on issues like onshore wind and investment zones that are receiving far less attention from commentators than they should further this point.

No matter the outcome of the reforms, this government will not always be in power. The tendency of the Labour alternatives to adopt growth as their goal has also only been strengthened in the weeks since my last blog post which highlighted comments from the Labour leader. While the pressures facing the UK are growing more acute, the intellectual direction of travel is toward caring about growth. The terms of the political debate have shifted in a positive direction. Economic growth is a moral issue which affects us all.

Ultimately the success or failure of the actions on Friday will be determined by the other reforms that this government is able to accomplish. The market reactions will likely make this more difficult. We should all hope that they succeed.

John Kroencke is a Senior Research Fellow at the Centre for Enterprise, Markets and Ethics. For more information about John please click here.

John Kroencke is a Senior Research Fellow at the Centre for Enterprise, Markets and Ethics. For more information about John please click here.

Graeme Leach, CEO & Chief Economist of Macronomics Consulting interviews Paul Williams, Professor of Marketplace Theology and Leadership at Regent College in Vancouver on the relationship between scripture and Economics.

Full video available below.

The longest reign of any British monarch came to an end on the afternoon of Thursday, September 8, 2022. Queen Elizabeth II died peacefully at Balmoral Castle, her favorite residence, in the northeast of Scotland. She occupied a unique place in the hearts of the British people and countless millions beyond the shores of the United Kingdom. We give thanks to God for her life and faith. May she rest in peace and rise in glory.

The implications of Her Majesty’s passing, for both the nation and the Church of England, are enormous. The Queen was a person of deep, personal, and genuine faith that expressed itself in numerous ways during the course of her reign. We will never see the like of her again. Her humility, not least in times of adversity, her cheerfulness as she carried out decades of public and charitable duties, and her absolute dedication to the service of the nation made her a focus of national unity and identity. We mourn her loss. She was deeply loved.

Quite simply it is impossible to overestimate the impact of Queen Elizabeth’s life and reign.

The future Queen was born in London on April 21, 1926. No one at that time could imagine that the Princess Elizabeth would go on to reign longer than any other British monarch, more than 70 years. Longer than the great Victoria (nearly 64 years), George III (just under 60 years), not to mention her namesake, Elizabeth I (a mere 44 years).

The British monarchy has never been devoid of complexity and trouble. When she was born, both her uncle and her father were in line for the throne before her, and any son born to her parents would also have taken precedence. It was never expected that she would succeed to the Crown. In 1936, upon the death of her grandfather, George V, her uncle Edward VIII was crowned king, only to abdicate to marry Wallis Simpson. The Church of England, of which Edward was titular head, would not allow the King to marry a divorced woman. And so Elizabeth’s father succeeded as George VI, and Elizabeth became heir presumptive.

The deep-rooted sense of service in Princess Elizabeth’s heart, her humility and sense of duty, was perhaps first broadcast more widely in her radio address on her 21st birthday in 1947.

I declare before you all that my whole life, whether it be long or short, shall be devoted to your service and the service of our great imperial family to which we all belong. But I shall not have strength to carry out this resolution alone unless you join with me, as I now invite you to do: I know that your support will be unfailingly given, God help me to make good my vow, and God bless all of you who are willing to share in it.

This really is a quite extraordinary statement of intent from someone so young. The themes of her future reign are clearly here for all to see: devotion, resolution, service, faith.

A few months later, on November 20, 1947, Elizabeth married Prince Philip of Greece and Denmark, later known as Philip Mountbatten, taking his mother’s name, and created Duke of Edinburgh on his marriage to the future Queen Elizabeth. They were married for 73 years, until his death on April 9, 2021. The image of Her Majesty alone at prayer in St. George’s Chapel, Windsor, at his funeral, dressed in black in the midst of the COVID-19 pandemic, became a defining image in the British political discourse of Boris Johnson’s premiership.

Elizabeth became Queen on February 6, 1952, at the age of 25, on the sudden death of her father. The King had been ill, treated for a malignant tumour. Elizabeth and Philip had set off on a tour to Australia, traveling via Kenya. The King was found dead in his bed in the early morning in his Norfolk residence at Sandringham, at the age of 56, after a coronary thrombosis. When he died, Elizabeth was asleep in the famous Treetops Hotel in Kenya. The news was conveyed to Prince Philip, who told Elizabeth when she awoke. They returned to London that same day, the Princess now Queen Elizabeth II, head of state and head of the commonwealth of nations. Without her consent, Parliament could not be summoned, no prime minister, other minister of the crown, judge, bishop, ambassador, or officer of the armed services appointed.

Six months before her coronation, Princess Elizabeth had stated:

Pray that God may give me wisdom and strength to carry out the solemn promises I shall be making, and that I may faithfully serve Him and you, all the days of my life.

The formal coronation took place on June 2, 1953. The Coronation Oath included the following faith commitment:

I will to the utmost of my power maintain the Laws of God and the true profession of the Gospel.

To that she remained faithful.

In 1955 the great evangelist Billy Graham visited London for one of his evangelistic crusades. Thousands were converted. The Queen met with the Southern Baptist preacher. The meeting was memorialized in the extraordinary, popular Netflix series The Crown, which proved an exceptionally engaging presentation of her life and reign. In actual fact, we do not know what the Queen and Billy Graham discussed; both had the maturity and discretion never to reveal the conversation. They almost certainly discussed forgiveness. Forty years later, on Easter Sunday 1995, Billy Graham preached in the Queen’s private chapel.

The Queen appointed 15 prime ministers—the last one, Liz Truss, just two days before her death. I list them to illustrate the mere passing terms of office of the political leaders compared to the constancy of Her Majesty; Winston Churchill (1951–55), Sir Anthony Eden (1955–57), Harold Macmillan (1957–63), Sir Alec Douglas-Home (1963–64), Harold Wilson (1964–70 and 1974–76), Edward Heath (1970–74), James Callaghan (1976–79), Margaret Thatcher (1979–90), John Major (1990–97), Tony Blair (1997–2007), Gordon Brown (2007–10), David Cameron (2010–16), Theresa May (2016–19), Boris Johnson (2019–22), and Liz Truss (2022–present). The longest of these was Margaret Thatcher, 11 years. The Queen reigned for 70.

Similarly, she met personally 12 U.S. presidents. Quite extraordinary.

Her own family presented many challenges. The failures of the marriages of three of her four children and the tragic death of Diana, Princess of Wales, caused her great pain and distress. Anne divorced in 1992, Charles and Andrew separated from their wives in that same year, which also saw a major fire at her beloved Windsor Castle. She described that year as her annus horribilis. Prince Andrew and Prince Harry have provided further challenges in more recent times.

Through it all, Elizabeth’s character was shaped by the Bible and her relationship with Jesus Christ, whose own life of sacrifice, service, and compassion formed the model and inspiration for her own. Throughout her life, the Queen consistently proclaimed the Christian gospel, which gave her strength, comfort, and peace. We saw this in so many ways, not least in her annual Christmas messages to the nation. Indeed, as time went on in the 2000s onward, she became ever more explicit in her faith. In 2002, she stated simply, “I draw strength from the message of hope in the Christian gospel.”

A fine example of her Christian witness is what she said in her 2011 broadcast:

God sent into the world a unique person—neither a philosopher nor a general, important though they are, but a Saviour, with the power to forgive.

And the following year:

This is the time of year when we remember that God sent his only Son “to serve, not to be served.” He restored love and service to the centre of our lives in the person of Jesus Christ.

You will read and hear numerous reflections on her reign. Her faith will be mentioned but not dwelt upon. I wanted to share with Acton readers the deeper expressions of her faith. I did not meet the Queen personally but saw her in the flesh on several occasions; at the services to open, and addresses to, the General Synod of the Church of England (on which I served for 10 years) and at the national Millennium Service in the year 2000. She was steadfast, dutiful, devoted, prayerful.

Shortly after the announcement of Her Majesty’s death, a rainbow, which promise of God’s faithfulness, appeared in the sky over Windsor Castle, the Queen’s main residence near London, followed by a double rainbow over Buckingham Palace. I am a sufficient believer in divine providence to assert this as a sign of God and an act of God.

What next? Many have dreaded this day. This is a moment of national sadness. This was a reign like no other. Many challenges lie ahead.

Charles III is now King. He will, in due course, take the Coronation Oaths. He will become Defender of the Faith. There was much discussion in earlier years that Charles wished to become Defender of Faith or even Faiths. Subtle distinctions go deep. The monarch is the Supreme Governor of the Church of England, a church that in its foundation documents makes clear is built on scripture and prayer. Charles’ faith is rather less explicit than that of the Queen. He is also divorced and remarried. The Church itself may wobble, no longer presided over by such a steadfast Christian as Queen Elizabeth, a Supreme Governor more faithful to Christ than any archbishop. We can only pray that Charles will come to know the Lord Jesus in the same way as did Her Majesty. There is also the politics. The Queen masterfully remained above the political fray; Charles has displayed a somewhat worrying tendency to meddle and, usually, in a progressive direction. Pray for restraint.

If there is one passage of Scripture that comes to mind upon reflecting on this momentous occasion, it is this:

I have fought the good fight, I have finished the race, I have kept the faith. Henceforth there is laid up for me the crown of righteousness, which the Lord, the righteous judge, will award to me on that day, and not only to me but also to all who have loved his appearing. (2 Tim. 4:7–8)

May I offer this prayer?

Gracious God, we give you thanks and praise for the life of your servant Queen Elizabeth, for her faith and her dedication to duty, to service and to nation. Bless us, our Father, as we mourn her death, and may her example continue to inspire us; through Jesus Christ our Lord. Amen.

God save the Queen. God save the King.

This article was first published for the Acton Institute.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.

Who can you trust to manage the public finances and cure inflation?

This is the key issue in this election campaign. Liz Truss wants to cut taxes, borrow more and start paying back after the next general election. Rishi Sunak wants to get inflation under control first as a foundation for enterprise and growth.

Sound money was key to Thatcherism. Mrs Thatcher saw inflation as a tax on every household and every business but a tax never passed by Parliament. For her inflation also had a moral dimension, as it does for Sunak. It penalises saving and pensions (other than index-linked pensions). It makes home ownership a pipe dream for younger people. It creates huge disparities of wealth. In addition inflation creates a culture of distrust which invariably leads to social conflict, witness current rail strikes and ballots for strike action in the public sector, the Don’t Pay campaign opposing rising energy bills and the disillusion of youth, saddled with repayment of university debts, forced to rent and a despairing economic outlook – the official Bank of England verdict.

Margaret Thatcher took a particular interest in Treasury affairs but she never looked at economic policy in isolation. Her policies were founded on her basic beliefs – telling the truth however unpalatable, balancing the books and personal values such as thrift, living within your means, hard work and self-reliance.

Over the five and a half years that I worked as head of the No 10 Policy Unit she would discuss government spending, borrowing and monetary conditions constantly. She had an instinctive grasp of economics and the need to ‘balance the books’ whether in business, in the family or in government.

I cannot count the number of times Mrs Thatcher told me that one of her greatest fears was that one day one of her Chancellors would cut taxes and “gamble on the future of the economy”.

Cutting taxes today is just such a gamble. It would reduce the country’s rainy-day reserves. We need reserves because of nasty surprises. Covid was a complete surprise. So was the Russian invasion of the Ukraine. So was Putin’s weaponisation of gas. So is the Chinese zero-Covid policy. We need reserves as a country much as we need reserves in families and businesses. As the Bank of England must raise interest rates to curtail spending, cutting taxes would mean greater government borrowing with higher debt interest payments. Tax cuts worsen the fiscal outlook without any direct impact on growth.

Increased business investment is critical to increasing growth. In making a decision to invest business is not so much interested in the next six to twelve months as in the next five to ten years. The key to that decision is what will happen to inflation. How far will it come down? Does anyone think it will come back to 2%? When inflation does come down how volatile will it be? The current inflation has shocked people. Consumer spending is falling. Until business and consumers know inflation has been beaten we will have stagflation.

For business inflation creates uncertainty over interest rates, the cost of capital, exchange rates, wage demands and output. And also the stability of government.

Mrs Thatcher practised what she preached. When she became Prime Minister she did not cut taxes in the 1979 budget, the month after being elected. Income tax was cut but VAT raised to offset it. In the 1980 budget taxes were not cut but modestly raised. In the 1981 budget taxes were not cut back but raised significantly. This was despite the objections of 364 economists at British universities signing a letter, drafted by two senior Cambridge professors of economics. In response, Professor Patrick Minford, who like me disagreed with the majority view, wrote in The Times (7 April 1981): “The essentials of the inflationary process are simple. It starts when government unwilling to cover expenditure by overt taxation and borrows from the public.”

Some economists advising Liz Truss judge that the situation today is different from Mrs Thatchers’s time, so it is possible for monetary policy to be tight and fiscal policy loose. They believe that the Bank of England already has inflation under control and should only start to pay back borrowing after the next election. Inflation was certainly higher in the early ’80’s than it is now but there is little evidence that people’s expectation of inflation or that the ambition of trade unions to claw back higher real wages is in any way diminished. Attempting to engineer tight money and loose public finances is a major gamble with our economy.

As someone who discussed economic policy with Mrs Thatcher frequently and at great length, it is inconceivable to me that she would ever have agreed to cut taxes at the present time. It was certainly her intention to cut taxes to create an enterprise economy but only when the time was right. At a time when public borrowing is 100% of GDP, annual interest on the debt alone is £80 billion, the labour market has more job vacancies than registered unemployed, the balance of payments deficit is very worrying, the pound shaky and inflation not just high (consumer price index 10.1%, retail price index 12.3%) but forecast to rise, the one thing we can say with certainty is that under these conditions Mrs Thatcher would never have cut taxes.

Cutting across the board taxes like national insurance and corporation tax today while inflation is soaring is no basis for future prosperity. Inflation is a punishing tax levied on every household and small business, made worse by the very tight labor market. Rishi Sunak is right to argue that cutting the inflation tax is the essential pre-requisite for sustained economic growth. We are facing tough times and the case against tax cutting is overwhelming.

Lord Griffiths is the Chairman of CEME. For more information please click here.

The confluence of events in the last few years have done no wonders for the economic performance of any country, but the longer-term performance of the British economy in the wake of the financial crisis is even more worrying. With the prospect of a sustained fall in real disposable income due to general inflation and, in particular, the severe rise in energy prices, the importance of renewed economic growth is only clearer. Indeed, we need to be clear that economic growth is a moral imperative. A growing economy is essential to the welfare and well-being of the whole nation, enabling all to flourish. Naturally, there will be political debate over the means and extent of the distribution or redistribution of the proceeds of growth, but the case for economic growth in principle needs to be made again and with clarity.

As Sam Ashworth Hayes argues by some measures the average employee earnings in the UK have never recovered since the financial crisis and won’t until at least 2027. One can debate the statistics but the fact that it is even debatable speaks volumes about recent economic performance. Other figures like the historic levels of taxation and the predicted steady rise in government spending in part due to demographic burdens only add to worries about the future.

It is easier to wish than to will, of course, but a clearly articulated vision for growth rather than managed decline or intentional degrowth is at the heart of a moral vision for the economy. With the defenestration of Boris (whose magical thinking applied to both national and personal finances) there are some signs of serious interest in economic growth by all the leadership candidates. Perhaps the most interesting was the now eliminated Kemi Badenoch who in her announcement said some interesting things about governing and economic performance in this context, one of which I reproduce below:

“Lower taxes yes, but to boost growth and productivity, and accompanied by tight spending discipline”.

The part I have italicized is important because it suggests an escape from both the more ideological support of all tax cuts and from bean-counting pessimism; deregulation and tax cuts in support of growth within the bounds of fiscal discipline. Stian Westlake, also in the Spectator, situates the more pessimistic attitude in the unique institution of the Treasury which combines budgetary, financial, and economic policymaking.This is unlike similar institutions in other countries where these roles are split among government agencies. As Westlake writes:

“The accountant mindset goes hand-in-hand with a historic pessimism about the government’s ability to improve the UK’s economic growth. The Treasury’s prior is that tax cuts, deregulation, public investment and other policy changes can do little to increase the UK’s rate of economic growth. Better the bird-in-the-hand of the tax increase or the spending cut today than the two-in-the-bush of higher national income.”

As a result of a similar assessment, Badenoch suggested splitting up the Treasury and creating a new office to focus on improving economic growth to in order to weaken the role of the Chancellor whose incentive for the accountant mindset “creates,” as Westlake writes, “a sort of learned helplessness in the rest of Whitehall that ends up costing the taxpayer more.”

One hopes that candidates for the highest office will reflect seriously on the opportunities for growth rather than simply continuing on with high spending, high tax and middling economic outcomes. Rishi Sunak, in his Mais Lecture suggests interest in reviving economic growth through some policy levers, but as Philip Salter wrote at the time there needs to be more work into the details (a point that applies to all candidates). The former Chancellor recently wrote that, “my ambition is that the UK should become by far the richest country in Europe within the next 15 years” before highlighting three areas of policy divergence with the EU that Brexit allows and that may enable growth.

It is a shame that it took the current situation to revive talk of economic growth, but thankfully arguments for economic growth are becoming more prominent among all plausible major candidates in the next general election (including Keir Starmer who recently said not only that “Labour will fight the next election on economic growth” but that “the first line of the first page of our offer will be about wealth creation”). Strange times, indeed. Of course, there are a great deal of hard-to-solve problems related to economic growth, but it is at least inspiring that there is more consensus about the major issue.

John Kroencke is a Research Fellow at the Centre for Enterprise, Markets and Ethics. For more information about John please click here.

Much of The Biblical Entrepreneur’s Experience comprises a rather simplistic and selective use of scripture to support a particular world-view, namely a North American free market system. As such, it could almost be categorised as espousing a prosperity gospel, in which correctly following biblical methods will necessarily bring success in business (see Chapter 2 for Davis’s “system”). The examples given in the book, of entrepreneurs such as Sarah Breedlove (Madam C.J. Walker), Strive Masiyiwa and Scott Harrison, tell this story in an often engaging way, but at times verge on a parody, which attempts to represent the complex riches of the Christian faith in an unreflective manner. One example is the song “The Hairdresser’s Ode to Madam C.J. Walker”, to the tune of “Onward, Christian Soldiers”, which the author cites approvingly (pages 72-73). The ‘mission’ of beautifying hair is conflated completely with the great Christian Commission in a manner that I found both disturbing and shallow.

Davis’s central metaphor, akin to a sermon illustration, is that of ‘bees and fleas’, and the author uses the bee/flea imagery to invite the reader into his world-view. BEEs (Biblical Experiential Entrepreneur) are good, and FLEAs (in-Flexible Learnt Entrepreneurial Antagonist) are bad. At the heart of Davis’s analysis is the proposition that “A BEE creates; a FLEA takes” (page 22). The book is peppered with “fun facts”, such as, “The honeybee has a heart!” (page 143), and side-bar notes, for example, “Strive – to devote serious effort or energy; to struggle in opposition” (page 115). Taken together, the above makes the overarching style of the book quite propositional and un-nuanced.

However, at times the book is also informative and every now and again I was pleased to find an interesting comment or statement that, I felt, contributed in a thoughtful way to a theological consideration of the subjects of enterprise and of entrepreneurial behaviour. For example, on the theme of entrepreneurial endeavour, Davis suggests: “It is to prepare the entrepreneur for the next life: a venture more fulfilling than its worldly counterparts” (page 5). This statement sketches out an idea which could be developed into some deep vocational thinking on the kingdom of heaven, and the place for enterprise within God’s enduring purposes. In another intriguing statement Davis comments: ‘…through grace we are given a great opportunity to provide others with a needed product or service to glorify Him – not ourselves” (page 11). Here, the themes of God’s grace, human need (not desire), and divine glory are all connected together under the umbrella of enterprise.

In Chapter 6 biblical examples are used to support the practice of “active listening”, as a way of harnessing God’s messages imparted through others, and Davis interestingly adds some thoughts about the challenges of fear and pride (pages 46-47). This “active listening” to others is to be set alongside the need for regular meditation on scripture (Chapter 15), not mere uncritical proof-texting, which appears elsewhere in the book. Separately, Chapter 10 plays with the “beehive” imagery and the way hexagons fit together perfectly, an illustration of how a project should work, a line of discussion that concludes with this communitarian statement: “…an individual cannot save the world; however a swarm of BEEs in each city can rebuild areas, then blocks of areas, followed quickly throughout a city. Multiple cities make up a country. Multiple countries make up a region. Multiple regions make up the world” (page 104).

A different book might have taken some of these statements and developed them by placing them alongside (and sometimes in tension with) the thinking set out by other authors who have considered the place for enterprise within the Christian world-view. The reader is left to do this work for themself. For example, the rich and in my mind helpful concept of the vocation of the entrepreneur, as proposed by Davis, could have been explored within a more general discussion on vocational calling, and specifically the nature of work within God’s providence.

In a way, the most inspiring section of this book for me was Section 6 (Chapters 16, 17 and 18), which describes empirical research about the distinctiveness of Christian-led and Christian-inspired businesses. Such enterprises typically have greater productivity, staff loyalty, and general outperformance. In this regard, I found the story of Walker Mowers engaging, not least the way in which the owners and directors of this business deliberately attempt to tell the story of the company within the bigger context of the story of salvation history (page 155). An enterprise is thus no longer a means to an end (profit), but is part of an over-arching narrative that embraces God’s purposes. This theme alone could have been developed into a major piece of thinking that I believe would be incredibly timely and helpful for business in today’s world.

In sum, this is a “popular” rather than “scholarly” book. It is, in the main, an easy read with occasional thought-provoking nuggets. With rather less “prosperity gospel” and rather more theological reflection on the important themes that are hinted at, it would have been much improved upon.

“The Biblical Entrepreneur’s Experience” by S Leigh Davis was published in 2021 by River Birch Press (ISBN-13: 9781951561802). 260pp.

Edward Carter is Vicar of St Peter Mancroft Church in Norwich, having previously been the Canon Theologian at Chelmsford Cathedral, a parish priest in Oxfordshire, a Minor Canon at St George’s Windsor and a curate in Norwich. Prior to ordination he worked for small companies and ran his own business.

Edward Carter is Vicar of St Peter Mancroft Church in Norwich, having previously been the Canon Theologian at Chelmsford Cathedral, a parish priest in Oxfordshire, a Minor Canon at St George’s Windsor and a curate in Norwich. Prior to ordination he worked for small companies and ran his own business.

He chairs the Church Investors Group, an ecumenical body that represents over £10bn of church money, and which engages with a wide range of publicly listed companies on ethical issues. His research interests include the theology of enterprise and of competition, and his hobbies include board-games, volleyball and film-making. He is married to Sarah and they have two adult sons.

French economist Philippe Aghion has long been associated with the model of growth through creative destruction – the so-called “Schumpeterian Paradigm”. In The Power of Creative Destruction he, together with his two French co-authors, seeks to summarise this paradigm and explain its implications. The authors believe, surely correctly, that “innovation and the diffusion of knowledge are at the heart of the growth process” (page 4) and they thus focus on the causes, impediments and consequences of innovation.

The scope of the book is vast and its pace breath-taking. The authors state that their purpose is to “Penetrate some of the great historical enigmas associated with the process of world growth… Revisit the great debates over innovation and growth in developed nations… [and] Rethink the role of the state and civil society” (page 2). The history of the world’s economy is reviewed in 20 pages and is followed by 13 further chapters dealing with issues as diverse as whether we should fear technological revolutions, whether competition is a good thing, the impact of innovation on inequality, whether developing countries can bypass industrialisation by moving immediately to a service economy, the impact of creative destruction on health and happiness, managing globalisation, the role of the state and the “golden triangle” of markets, state, and civil society. All this in 319 pages!

Inevitably, the result is broad but shallow and the reader’s reaction to it will depend upon what they are looking for. Those seeking insights based on new original research or indepth analysis of issues and carefully argued conclusions should look elsewhere, perhaps to some of Philippe Aghion’s other works; on the other hand, those who wish to think about a broad range of issues and to have some previously unexamined assumptions challenged will find the book stimulating and, probably, an inspiration for further exploration.

It is based on the authors’ lectures at the College de France and it could well serve as a student text. However, the preface strongly suggests that the real target audience is policymakers: it contains much advice, even instructions, for Western Governments, of which perhaps the most stern is that “they must accompany the process of creative destruction, without obstructing it” (page vii).

The book was written between late 2019 and mid 2020 against the background of the Covid pandemic. The authors suggest that the pandemic has acted “as a wake-up call by revealing deeper problems that plague capitalism” (page vii) and they argue that what is required is a reformation of capitalism. So many recent books have adopted this starting point that there is a danger of it being greeted with a yawn and the expectation that what will follow will comprise the standard left-wing prescription of more government intervention and redistributive taxation. However, as the emphasis on creative destruction should suggest, this is not what Philippe Aghion and his colleagues advocate.

They see a role for the state that is larger than that which many free market economists would support. In particular, they see a role for it in financing and generally promoting the development of certain technologies that might otherwise not be developed (particularly those associated with the transition to a low carbon economy). However, they accept that “Objections to industrial policy from the 1950s through to the 1980s are difficult to counter, all the more because later work, such as that of Jean-Jacques Laffont and Jean Tirole, pointed to several sources of inefficiency in state intervention” (page 68). In particular, they recognise that national industrial policy has the effect of limiting or distorting competition, that governments are not great at picking winners and that governments may be receptive to lobbying by large incumbent firms. Consequently, they recognise that we must look primarily to the market rather than to governments to secure economic prosperity.

Some parts of The Power of Creative Destruction are basic, even to the point of distortion. For example, the description of the drivers of the industrial revolution is hopelessly superficial and does not even consider the role of beliefs, ideas and culture (which Deirdre McClosky has analysed so carefully in Bourgeois Equality). There are also some irritating inaccuracies in the book. For example, James Watt did not invent the steam engine (as is stated on page 40), the wheel was not invented in China (as is wrongly stated on page 20) but most likely in Eastern Europe and there was no “year zero” (which is bizarrely referred to on both page 22 and page 26). However, these errors are minor and the book contains a lot that is of real substance. Most readers will, at the very least, find thought provoking material within it.

For example, the authors draw attention to a number of studies that should at least cause pause for thought among those who see greater equality and better social outcomes coming primarily from government action: a comparison among different American states that suggests that innovation increases “both the share of income of the richest 1% (top income in equality) and social mobility” (page 82); other evidence points to a very strong positive correlation between job creation and job destruction (i.e. that the preservation of “zombie” corporations is an obstacle to the creation of new jobs; page 214ff); and evidence from Finland suggests that parental influence remains a decisive factor in whether a child will become an innovator even in a country where the educational system is highly egalitarian and of high quality (page 199ff).

Other parts of the book presents challenges to those who favour less government intervention. For example, the authors present evidence that “strongly suggests that as a firm gains greater market power and moves towards market dominance, it focuses its efforts less and less on innovation and more and more on political connections and lobbying” (page 92). There are also some tantalisingly brief policy suggestions, perhaps the most interesting of which is the idea (originally put forward by Richard Gilbert in Innovation Matters) that antitrust authorities need to change the way that they look at mergers by not using the definition of existing markets as their loadstar and instead evaluating the extent to which a merger could discourage the entry of new innovative firms (page 123).

Much of the evidence supporting these assertions and suggestions is set out in innumerable graphs. These are interesting and informative but a few words of warning need to be sounded: the graphs require careful study and this is rendered more difficult in some cases by the inadequacies of their labelling; furthermore, in a number of cases, it is difficult properly to understand and evaluate the relevant graph without access to the book or paper from which it has been extracted.

More generally readers need to be careful that the readability of the text does not cause them to be swept along by the authors and fail to spot the points at which the evidence presented fails adequately to support the argument being made. This is not to say that the relevant arguments are wrong but merely to warn that, in many cases, the authors have not proved that they are right.

That said, The Power of Creative Destruction is a good read: it avoids overly technical language, does not assume a lot of prior knowledge, has been well translated by Jodie Cohen-Tanugi and clearly presents important ideas.

“The Power of Creative Destruction: Economic Upheaval and the Wealth of Nations” by Philippe Aghion, Céline Antonin and Simon Bunel was published in 2021 by The Belknap Press of Harvard University Press (ISBN-13:9780674971165).319pp

Richard Godden is a Lawyer and has been a Partner with Linklaters for over 25 years during which time he has advised on a wide range of transactions and issues in various parts of the world.

Richard’s experience includes his time as Secretary at the UK Takeover Panel and a secondment to Linklaters’ Hong Kong office. He also served as Global Head of Client Sectors, responsible for Linklaters’ industry sector groups, and was a member of the Global Executive Committee.

On Wednesday 6th July 2022 the Centre for Enterprise, Markets and Ethics (CEME) and the Institute of Economic Affairs (IEA) hosted a joint event to discuss the topical question of whether the UK public has lost faith in free markets, and if so what might be done about it.

CEME’s Director, Revd Dr Richard Turnbull, presented startling polling undertaken by CEME which reveals that the general public and churchgoers views of the market differ dramatically from those of the elites in business or the church and considers what this might signal. Has business lost confidence in business?

The event was chaired by Lord Griffiths of Fforestfach.

The economic headwinds facing Britain seem to be evermore penetrating – recently we have seen:

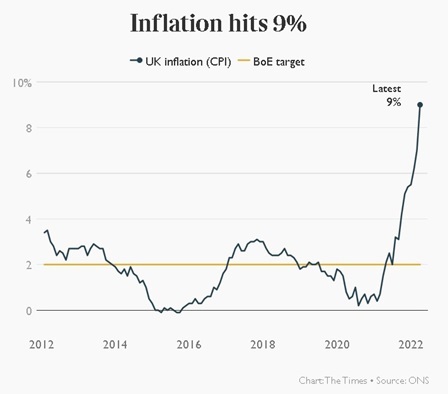

Inflation hit a 40-year high of 9%

Largely driven by the increase in utility prices and the higher energy price cap that came into effect (see chart below). ONS chief economist, Grant Fitzner said that, “Around three quarters of the increase in the annual rate [of inflation] this month came from utility bills.” CEME Chairman Brian Griffiths has written extensively on the issue and has warned on repeated occasions about the threat and ills of inflation. In his first article entitled The Spectre of Inflation written back in August 2020 he wrote that,

“We must take the prospect of inflation seriously. […] To allow inflation to rise would be a failure to learn the lessons of history. […] Controlling inflation is painful. It requires the central bank to raise interest rates. […] Each time interest rates have been raised, inflation has been brought down, but only at the cost of increased unemployment”.

The markets have seen their biggest drop since the pandemic began in March 2020

Two years later and we are very much in this ‘painful’ phase of stemming inflationary prices through (an increasingly) contractionary monetary policy. Yet, we are only at the start of beginning to feel the economic and social consequences of rising interest rates.

The S&P 500 briefly fell into bear market territory dropping more than 20% since its previous record high. £40bn has been wiped off the FTSE 100 intensifying fears that the UK is heading for a recession. The online news outlet and portal ThisIsMoney asks, “Is a recession inevitable as inflation hammers the UK and interest rates are hiked?”

Energy prices of course have reached record highs rising by 54% in April 2022 alone

The average household currently pays just under £2,000 in annual energy bills but modelling conducted by E.ON suggests this could rise to £3,000 by October 2022. Ofgem Chief Executive Jonathan Brearley confirmed that energy prices will likely hit £2,800 this year and that this is a “once in a generation event not seen since the oil crisis in the 1970s”. Lower income households may be faced with spending as much as 40% of their disposable income on energy, leaving millions of people in fuel poverty (as many as 12 million according to Mr Brearley).

What does this mean for savings?

At first glance, rising prices will mean that households and in particular those on low incomes may find themselves having to ‘break the piggy bank’ to make ends meet. That is of course, if they are in the more fortunate position of having a piggy bank in the first place. For many, it will mean sacrificing long-term funds for short-term survival – placing households in the potentially tr situation of having no financial resources at all. Worse yet, some will be forced to take on additional debt that may prove unsustainable, meaning that families and individuals could rather quickly find themselves in a dangerous financial pit.

The most recent Quarterly Outlook (May 22’) of the National Institute of Economic and Social Research (NIESR) found that, “1.5 million households (5% of the population) have food and energy bills greater than their disposable income. For these households, who likely do not have sufficient savings or access to credit cards to help them cope with these prices, we can expect them to either resort to payday loans, or simply not pay their bills by going into arrears and incurring more long-term debt.”

So those with savings are facing a difficult challenge. Inflationary pressures will continue to reduce the value of existing savings over time and rising costs are forcing more and more households to dip into savings for their daily sustenance. The savings ratio has plummeted from the pandemic high of 23.9% in Q2 of 2020 to 6.8% in Q4 of 2021 (ONS) – we can only expect this to drop further.

There are no easy solutions to this complex post-pandemic economic environment. In the short-to-medium term inflation has to be brought down, meaning that the BOE will have to continue to rise interest rates. Yet this may also be an opportune moment for the Treasury to reverse some of the previous National Insurance hikes and offer a tax cut to the working population and business in general (perhaps a reduction in VAT seems appropriate?). This would not only send the right message to the markets, it would also boost confidence and offer many small to medium-sized enterprises a much needed lifeline to counter rapidly spiralling costs.

Supply side fiscal responses proved successful in the Ragan/Thatcher era of the 70s and 80s. The Federal Reserve under Paul Volker brought down US inflation from 13.5% in 1980 to 4.1% in 1988 (interest rates remained relatively high throughout the 80s), whilst ‘Reaganomics’ promoted economic growth. GDP under the Reagan Administration averaged 3.5%; compared to George H.W. Bush at 2.25%; Bill Clinton 3.88%, George W. Bush 2.2% and Barack Obama 1.62%. Similarly, inflation in the UK under Thatcher dropped from almost 18% in 1980 to around 3% in 1987.

Quick and sustained action is needed to bring down inflation. Higher interest rates need to be balanced with supply-side policies. It is unfortunate that the tax burden has reached its highest level in 70 years under a Conservative government, while many are struggling to afford the daily basics. The problem is that the Conservatives risk losing their once-held credibility on economic matters as the former Brexit Secretary David Davies pointed out, “It’s a real risk now that the party is going to lose its reputation for economic competence.” The tide must be turned before it is too late.

Andrei E. Rogobete is Associate Director at the Centre for Enterprise, Markets & Ethics. For more information about Andrei please click here.

UK inflation is at a 40-year high and rising. The consumer price index has hit 9%, the retail price index 11.1%. As the Government’s official target is 2%, the blame game is in full swing, with the main target being Bank of England and its Governor, Andrew Bailey.

The Government’s priorities, outlined in the recent Queen’s Speech, are “strengthening growth and easing the cost of living”. That is something we can all agree with. It means better housing, better public services, making a reality — not simply an aspiration — of levelling up, reducing inflation and helping those squeezed by the rising cost of living.

If these objectives are to be realised, one requirement has to be met.

Inflation must be brought back down to 2%, the Government must endorse 2% as the target going forward and, most importantly, it must be delivered. This cannot happen immediately, but the Bank states in its recent Monetary Policy Report that it can be achieved by 2024.

The rising cost of living is now the number one challenge facing the Government. It is proving painful for most people, but extremely painful for the least well off. We have all heard or read stories of so many families who are desperately trying to help their children and themselves just to bring food to the table. Fuel poverty has already hit 20% of households and is predicted to rise to 40%.

Inflation is clearly painful, but it is more than just a painful economic shock.

Inflation is a corrosive force in our society. It creates suspicion, distrust and social conflict. It produces a blame culture, which undermines trust. People think the local corner shop is just jacking up prices to do them down, just like the large electricity companies. The same applies to Shell and BP who have done nothing special to earn the massive rise in profits. Supermarkets are no different. Why is Waitrose increasing prices much more than Aldi and Lidl? Inflation breeds a culture of blame, resentment and distrust. The threatened strike by RMT, the rail union, later this summer, could well become a landmark for higher wage settlements and a signal that stagflation may not be a temporary phenomenon.

The prospect of a windfall tax on the excess profits, not just of gas and oil producers but electricity generators, including wind farms operators, has needlessly infuriated these companies. This creates uncertainty, hits business confidence and will raise the cost of capital for investors. Multinational companies may well prefer to invest elsewhere.

Tackling inflation is where the Bank of England comes into the picture.

When the Covid pandemic hit the UK at the start of 2020, nearly everyone was supportive of the Bank of England slashing interest rates to 0.1%, increasing monetary growth and supporting businesses with easy credit. The objective was to avoid another Great Depression like that of the 1930s: falling prices, mass unemployment and business failures. I supported the Bank pursuing this objective, not least by increasing money supply growth to finance increased spending on the NHS, the furlough employment scheme and providing more credit at cheap rates for businesses.

However, already by the late summer of 2020 there were signs that the policy was giving a lift to the economy: company sales were rising briskly, corporate profits increasing and prices in assets which were hedges against inflation taking off, such as gold and precious metals, commodities, o bjet s d’arts , even Michael Jordan’s basketball shoes.

Back in August 2020, I wrote an article here , “The spectre of inflation”, which argued that we were in danger of creating too much money for the supply of goods and services available. I followed it up last year with four more articles for TheArticle, criticising the Bank for not raising interest rates and urging action.

Unfortunately, last year the Bank made a serious policy error which consisted of keeping interest rates very low and through Quantitative Easing buying government stock in the market and increasing money growth, while insisting that inflation was “transitory”.

With inflation now at 9%, the Bank of England and the Governor, Andrew Bailey, have taken a hammering from backbench MPs, in the House of Lords debate and from numerous commentators. Frankly, I have been surprised at the ferocity of the attacks in the middle of a debate in the Lords and changed the content of my speech there because I felt that we were beginning to play the man (Bailey) and the institution (the Bank), not the ball.

In the Bank’s defence

To start with I do not believe that the Bank or the Governor were “asleep at the wheel”.

The pandemic was an extraordinary event with a series of new variants of the Covid virus, a series of lockdowns and genuine uncertainty as to how exactly the economy was behaving. The fall in output was the worst recorded in 300 years. The lockdowns were more severe than during any of the wars in our history. Next, there was considerable uncertainty over the extent of the true measure of unemployment, as it was disguised by the furlough scheme. As is clear from the evidence given by members of the Monetary Policy Committee to the Treasury Select Committee (9 May 2022), their so-called “dithering” over whether to raise interest rates in November 2021 was simply their collective caution because the furlough scheme had only come to an end the previous month.

Meanwhile throughout the whole of this 18-month period, other central banks, such as the US Federal Reserve and the European Central Bank, were (like the Bank of England) convinced that the increase in inflation was “transitory” and would of itself come down soon. They were advancing similar arguments to the Bank of England. Some allowance should also be made for the fact that hardly anyone on the Bank’s staff had lived through the inflation of the 1970s.

The one criticism therefore that does not hold any water is that they were “asleep at the wheel”.

In addition, for most of the period up to November 2021 most commentators had not been calling for the Bank to raise interest rates. They were very happy with forecasts which showed a remarkable economic recovery and their major concern was that they did not wish to see it jeopardised by higher interest rates. The outcome they feared most was not inflation but recession.

The Bank’s defence of its policies was weakened by three other factors.

First, there has been a lack of intellectual diversity among members of the Monetary Policy Committee. With rare exceptions they have all accepted the New Keynesian framework in which policy has been conducted. This has resulted in underestimating the genuine uncertainty facing policymakers in the world in which we live. They have highly emphasised the importance of the expectations of inflation held by consumers, businesses and investors, but have misled themselves into believing that by issuing “forward guidance” about what is really taking place in the economy and through the powerful toolkit at their disposal (changing interest rates and buying and selling government stock), they could thereby control inflation.

Second, there has been groupthink among central banks. They meet monthly at the Bank for International Settlements in Basel and in any case can talk to each other at any time. The result has been that all of the leading central banks employ the same intellectual framework.

Third, the Bank of England has as its primary goal the control of inflation. However, it has numerous other secondary objectives: stability of the financial system, support for the government of the day’s economic policy, specifically growth and employment, the soundness of firms, ensuring competitive markets in the financial sector and most recently the resilience of the financial system to reach to net zero. Certain of these objectives clash with each other and so the Bank has to make a judgement on trade-offs. The result is that instead of always looking ahead, it has to look sideways to find out the public’s likely response to such things as higher mortgage rates, a slowing growth rate, rising unemployment, or progress towards net zero.

Neglect of money

The major failure of the Bank, however, is none of these but an intellectual error, namely the neglect of money growth as one key determinant of inflation. Far from being asleep at the wheel, those in the driving seat have 100% focused on the journey, the vehicle has been in fine condition, all the controls have been working well, but they have been using the wrong map and handbook.

The importance of money growth in understanding any sustained bout of inflation is in my judgement beyond dispute. Even those who recognise the importance of money (“monetarists”) recognise its limitations. For example, Milton Friedman wrote:

“The proposition that inflation is a monetary phenomenon is important yet it is only the beginning of an answer to the causes of and cures of inflation… because the deeper question is why excessive monetary growth occurs”. (Milton and Rose Friedman, Free to Choose p. 264, Secker & Warburg 1980, London)

In a similar vein, Friedrich Hayek argued: “I will admit that in its classic form, as now revived by my friend, Milton Friedman, this theory [monetarism] grossly oversimplifies things by making it all an issue of statistical aggregates and averages.” (Commentary, the Times, 28 March 1980)

This is particularly true at present when there is such uncertainty over the likely course of policy making and shortages, sanctions and tight labour markets all of which affect aggregate output.

There is also one further but important conversation.

The Bank of England was established over 300 years ago and has served us well. It has avoided hyper-inflation during times of war, unlike many other European countries and until it was nationalised in 1946 the Bank was entirely independent of government. It was only 25 years ago that it was given back operational independence. It is a venerable institution and one of the pillars of our unwritten constitution. As Lord Fox, the Liberal Democrat peer, said in a recent debate in the House of Lords: “We have to be careful not to undermine — or to set in train a process that undermines [an independent Bank of England]. We… have a duty of care around this issue.” (Hansard Vol 822 No 4, 16 May 2022.)

The current lapse in performance by the Bank is no reason for the Treasury to take back control. It is they, after all, who have appointed members of the Monetary Policy Committee.

When in the 1970s the Bank increased money growth to finance the Barber Boom and facilitate our entry into the European Economic Community, the blame for the inflation lay solely with politicians. The Chancellor was the key person responsible for setting the level of Bank rate and effectively the conduct of monetary policy. Today it is not the politicians who are first in the firing line, but the Governor of the Bank of England and the Bank itself.

While no individual or institution is beyond criticism, because of the Bank’s standing in our unwritten constitution and the status of its staff as unelected public servants who cannot say everything they might wish to, we do have a duty of care.

In my judgement the tone recently has become uncomfortable. Instead, the focus of comment should be on three issues.

1. We should be strengthening the resolve of the Bank to act now to raise interest rates. At present the real rate of interest (i.e. Bank rate adjusted for inflation) stands at negative 8%: this has put us on the road to stagflation along which we are travelling. A rise in rates to whatever level is necessary will change people’s expectations of inflation.

2. Everyone would like to avoid a recession. The best way to limit the impact of a recession is by rising rates now to whatever level is necessary, so that people become convinced that inflation will be brought under control.

3. The fiscal boost to household spending just announced by the Chancellor, coupled with a very tight labour market, is a window of opportunity for the Bank to act.

This article was first published in TheArticle.

Lord Griffiths is the Chairman of CEME. For more information please click here.