UK inflation is at a 40-year high and rising. The consumer price index has hit 9%, the retail price index 11.1%. As the Government’s official target is 2%, the blame game is in full swing, with the main target being Bank of England and its Governor, Andrew Bailey.

The Government’s priorities, outlined in the recent Queen’s Speech, are “strengthening growth and easing the cost of living”. That is something we can all agree with. It means better housing, better public services, making a reality — not simply an aspiration — of levelling up, reducing inflation and helping those squeezed by the rising cost of living.

If these objectives are to be realised, one requirement has to be met.

Inflation must be brought back down to 2%, the Government must endorse 2% as the target going forward and, most importantly, it must be delivered. This cannot happen immediately, but the Bank states in its recent Monetary Policy Report that it can be achieved by 2024.

The rising cost of living is now the number one challenge facing the Government. It is proving painful for most people, but extremely painful for the least well off. We have all heard or read stories of so many families who are desperately trying to help their children and themselves just to bring food to the table. Fuel poverty has already hit 20% of households and is predicted to rise to 40%.

Inflation is clearly painful, but it is more than just a painful economic shock.

Inflation is a corrosive force in our society. It creates suspicion, distrust and social conflict. It produces a blame culture, which undermines trust. People think the local corner shop is just jacking up prices to do them down, just like the large electricity companies. The same applies to Shell and BP who have done nothing special to earn the massive rise in profits. Supermarkets are no different. Why is Waitrose increasing prices much more than Aldi and Lidl? Inflation breeds a culture of blame, resentment and distrust. The threatened strike by RMT, the rail union, later this summer, could well become a landmark for higher wage settlements and a signal that stagflation may not be a temporary phenomenon.

The prospect of a windfall tax on the excess profits, not just of gas and oil producers but electricity generators, including wind farms operators, has needlessly infuriated these companies. This creates uncertainty, hits business confidence and will raise the cost of capital for investors. Multinational companies may well prefer to invest elsewhere.

Tackling inflation is where the Bank of England comes into the picture.

When the Covid pandemic hit the UK at the start of 2020, nearly everyone was supportive of the Bank of England slashing interest rates to 0.1%, increasing monetary growth and supporting businesses with easy credit. The objective was to avoid another Great Depression like that of the 1930s: falling prices, mass unemployment and business failures. I supported the Bank pursuing this objective, not least by increasing money supply growth to finance increased spending on the NHS, the furlough employment scheme and providing more credit at cheap rates for businesses.

However, already by the late summer of 2020 there were signs that the policy was giving a lift to the economy: company sales were rising briskly, corporate profits increasing and prices in assets which were hedges against inflation taking off, such as gold and precious metals, commodities, o bjet s d’arts , even Michael Jordan’s basketball shoes.

Back in August 2020, I wrote an article here , “The spectre of inflation”, which argued that we were in danger of creating too much money for the supply of goods and services available. I followed it up last year with four more articles for TheArticle, criticising the Bank for not raising interest rates and urging action.

Unfortunately, last year the Bank made a serious policy error which consisted of keeping interest rates very low and through Quantitative Easing buying government stock in the market and increasing money growth, while insisting that inflation was “transitory”.

With inflation now at 9%, the Bank of England and the Governor, Andrew Bailey, have taken a hammering from backbench MPs, in the House of Lords debate and from numerous commentators. Frankly, I have been surprised at the ferocity of the attacks in the middle of a debate in the Lords and changed the content of my speech there because I felt that we were beginning to play the man (Bailey) and the institution (the Bank), not the ball.

In the Bank’s defence

To start with I do not believe that the Bank or the Governor were “asleep at the wheel”.

The pandemic was an extraordinary event with a series of new variants of the Covid virus, a series of lockdowns and genuine uncertainty as to how exactly the economy was behaving. The fall in output was the worst recorded in 300 years. The lockdowns were more severe than during any of the wars in our history. Next, there was considerable uncertainty over the extent of the true measure of unemployment, as it was disguised by the furlough scheme. As is clear from the evidence given by members of the Monetary Policy Committee to the Treasury Select Committee (9 May 2022), their so-called “dithering” over whether to raise interest rates in November 2021 was simply their collective caution because the furlough scheme had only come to an end the previous month.

Meanwhile throughout the whole of this 18-month period, other central banks, such as the US Federal Reserve and the European Central Bank, were (like the Bank of England) convinced that the increase in inflation was “transitory” and would of itself come down soon. They were advancing similar arguments to the Bank of England. Some allowance should also be made for the fact that hardly anyone on the Bank’s staff had lived through the inflation of the 1970s.

The one criticism therefore that does not hold any water is that they were “asleep at the wheel”.

In addition, for most of the period up to November 2021 most commentators had not been calling for the Bank to raise interest rates. They were very happy with forecasts which showed a remarkable economic recovery and their major concern was that they did not wish to see it jeopardised by higher interest rates. The outcome they feared most was not inflation but recession.

The Bank’s defence of its policies was weakened by three other factors.

First, there has been a lack of intellectual diversity among members of the Monetary Policy Committee. With rare exceptions they have all accepted the New Keynesian framework in which policy has been conducted. This has resulted in underestimating the genuine uncertainty facing policymakers in the world in which we live. They have highly emphasised the importance of the expectations of inflation held by consumers, businesses and investors, but have misled themselves into believing that by issuing “forward guidance” about what is really taking place in the economy and through the powerful toolkit at their disposal (changing interest rates and buying and selling government stock), they could thereby control inflation.

Second, there has been groupthink among central banks. They meet monthly at the Bank for International Settlements in Basel and in any case can talk to each other at any time. The result has been that all of the leading central banks employ the same intellectual framework.

Third, the Bank of England has as its primary goal the control of inflation. However, it has numerous other secondary objectives: stability of the financial system, support for the government of the day’s economic policy, specifically growth and employment, the soundness of firms, ensuring competitive markets in the financial sector and most recently the resilience of the financial system to reach to net zero. Certain of these objectives clash with each other and so the Bank has to make a judgement on trade-offs. The result is that instead of always looking ahead, it has to look sideways to find out the public’s likely response to such things as higher mortgage rates, a slowing growth rate, rising unemployment, or progress towards net zero.

Neglect of money

The major failure of the Bank, however, is none of these but an intellectual error, namely the neglect of money growth as one key determinant of inflation. Far from being asleep at the wheel, those in the driving seat have 100% focused on the journey, the vehicle has been in fine condition, all the controls have been working well, but they have been using the wrong map and handbook.

The importance of money growth in understanding any sustained bout of inflation is in my judgement beyond dispute. Even those who recognise the importance of money (“monetarists”) recognise its limitations. For example, Milton Friedman wrote:

“The proposition that inflation is a monetary phenomenon is important yet it is only the beginning of an answer to the causes of and cures of inflation… because the deeper question is why excessive monetary growth occurs”. (Milton and Rose Friedman, Free to Choose p. 264, Secker & Warburg 1980, London)

In a similar vein, Friedrich Hayek argued: “I will admit that in its classic form, as now revived by my friend, Milton Friedman, this theory [monetarism] grossly oversimplifies things by making it all an issue of statistical aggregates and averages.” (Commentary, the Times, 28 March 1980)

This is particularly true at present when there is such uncertainty over the likely course of policy making and shortages, sanctions and tight labour markets all of which affect aggregate output.

There is also one further but important conversation.

The Bank of England was established over 300 years ago and has served us well. It has avoided hyper-inflation during times of war, unlike many other European countries and until it was nationalised in 1946 the Bank was entirely independent of government. It was only 25 years ago that it was given back operational independence. It is a venerable institution and one of the pillars of our unwritten constitution. As Lord Fox, the Liberal Democrat peer, said in a recent debate in the House of Lords: “We have to be careful not to undermine — or to set in train a process that undermines [an independent Bank of England]. We… have a duty of care around this issue.” (Hansard Vol 822 No 4, 16 May 2022.)

The current lapse in performance by the Bank is no reason for the Treasury to take back control. It is they, after all, who have appointed members of the Monetary Policy Committee.

When in the 1970s the Bank increased money growth to finance the Barber Boom and facilitate our entry into the European Economic Community, the blame for the inflation lay solely with politicians. The Chancellor was the key person responsible for setting the level of Bank rate and effectively the conduct of monetary policy. Today it is not the politicians who are first in the firing line, but the Governor of the Bank of England and the Bank itself.

While no individual or institution is beyond criticism, because of the Bank’s standing in our unwritten constitution and the status of its staff as unelected public servants who cannot say everything they might wish to, we do have a duty of care.

In my judgement the tone recently has become uncomfortable. Instead, the focus of comment should be on three issues.

1. We should be strengthening the resolve of the Bank to act now to raise interest rates. At present the real rate of interest (i.e. Bank rate adjusted for inflation) stands at negative 8%: this has put us on the road to stagflation along which we are travelling. A rise in rates to whatever level is necessary will change people’s expectations of inflation.

2. Everyone would like to avoid a recession. The best way to limit the impact of a recession is by rising rates now to whatever level is necessary, so that people become convinced that inflation will be brought under control.

3. The fiscal boost to household spending just announced by the Chancellor, coupled with a very tight labour market, is a window of opportunity for the Bank to act.

This article was first published in TheArticle.

Lord Griffiths is the Chairman of CEME. For more information please click here.

Thomas Macaulay observed that “Free trade, one of the greatest blessings which a government can confer on a people, is in almost every country unpopular.”. There is plenty of evidence to support this assertion but the reason for public hostility is less clear. What is it that impacts public opinion about trade and why is it not better liked?

Diana Mutz, Professor of Political Science and Communications at the University of Pennsylvania, has spent a number of years researching these questions in the United States and, in Winners and Losers: The psychology of foreign trade, she summarises the results of her research, considers the evidence of other researchers, draws conclusions and reflects upon their implications. She says that her “central purpose … is to bridge a gap in our understanding of the causes and consequences of American attitudes toward international trade” (page 15).

The result is both fascinating and important. All those who believe in the merits of free trade and wish to see it widely pursued by democratic countries should read what Mutz has to say.

She begins with three basic propositions, each of which she successfully justifies. First, “for most Americans, globalization is something happening ‘out there’, away from their everyday lives” (page 2). Secondly, unsurprisingly, most Americans are largely unaware of the economic arguments for and against free trade. As Mutz puts it, “few wax poetic about the wonders of the invisible hand, the efficiency of market specialization, or even the lower cost of consumer goods” (page 3). Thirdly, despite their profound ignorance, people do nonetheless hold opinions about international trade, holding “alternative, lay theories about how international trade works” (page 3).

Many economists have asserted that these home-spun theories are based on the self-interest and Milton Friedman asserted that “Complete free trade is not politically feasible … because it is only in the general interest and in no-one’s special interest”. Mutz’s research, however, provides little support for this. Instead, she suggests that public opinion is based upon sociotropic factors or what, more bluntly, might be called unsophisticated nationalism.

Mutz observes that trade is often seen in terms of competition rather than cooperation and American attitudes to trade are determined to a considerable extent by whether or not it is expected that America will be the “winner”. Furthermore, many people perceive trade as a zero sum game in relation to job gains and losses and, when coupled with uncertainty as to whether America will be the “winner”, this perception can produce highly negative attitudes to it.

Mutz suggests that people’s reasoning in relation to trade is similar to their reasoning in relation to human relationships at a personal level: “People trust people who look more like them” (page 101) and people are influenced by things as basic as who they like and who they do not like. Hence, in a survey conducted by Mutz, those who, in answer to a request to name the US’s three largest trading partners forgot Canada were less likely to support international trade than those who remembered Canada, whilst those who forgot China were more likely to support trade than those who remembered it.

Unfortunately, all of the attitudes that lead to a negative view of trade receive regular reinforcement. Mutz’s survey of references to trade in major US newspapers between 2000 and 2018 indicates that the vast majority of such references viewed trade as competition rather than cooperation; her survey of references to job losses in major US newspapers over the same period indicates that trade is frequently blamed for losses, whilst automation is very rarely blamed despite most economists believing that this is the primary cause of US manufacturing job loss; the idea of trade being a zero sum game is reinforced by concepts such as “trade deficits” and even “fair trade” (which sound, to the uninitiated, as though a fixed sized pie is being unevenly divided); and news stories reporting the benefits of free trade generally support their narrative with graphs and other impersonal material whilst those opposing it show pictures of forlorn American workers who have lost their jobs, which naturally have a bigger emotional impact. More fundamentally, Mutz points to the simplicity of the claims made by those who oppose free trade (primarily relating to job losses) in comparison to the complexity of the arguments in favour of free trade.

Mutz provides copious evidence that, overall, supports her theories. However, the book is not without flaw. Some of the numerous graphs and charts are not well labelled and space limitations have resulted in Mutz cross referring to a significant amount of online material. Readers also need to be on their guard since a number of the graphs are not based to zero, which results in differences being exaggerated (the graphs on page 127 relating to racial differences being particularly egregious examples of this). Furthermore, some of the research results, whilst statistically significant, do not suggest huge differences among different categories of people and Mutz may on occasions be guilty of over-interpreting them.

Mutz is clearly highly pro trade and moderately to the left of centre in her political views. She does not disguise her distaste for some of those who take a different view and, unfortunately, this may have distorted some of her conclusions. For example, she appears to believe that those who are pro trade are more rational than those who oppose it but this does not seem consistent with her own evidence. Thus, she comments that “protectionist attitudes in the US are driven largely by non-economic, symbolic beliefs” (page 241) apparently forgetting that the same appears to be true of attitudes that favour free trade. She also appears reluctant to acknowledge that some non-economic arguments relating to trade may be rational and reasonable. For example, no matter how pro free trade one might be, it is hard to disagree that there are downsides in trading with countries governed by authoritarian regimes and thus the apparent implication in Mutz’s comments that logical and reasonable people should favour trade with China as much as they favour trade with Canada is surely misplaced.

Mutz recognises that her findings are limited to the USA and her evidence from Canada suggests that they may not apply elsewhere. Nonetheless, the findings present those who favour free trade with a challenge: what are we to do about this? Mutz makes a number of reasonable suggestions: efforts should be made to make people realise that most job losses are not caused by trade but by automation; we need to make efforts to enable people to understand trade in terms of cooperation and to realise that it is not a zero sum game; and we need to build on the finding that the vast majority of Americans believe that trade is good for relationships with other countries. However, these suggestions are vague and do not relate closely to all of the issues that Mutz identifies.

In particular, she fails to focus adequately on her recognition that many influences on people’s attitude to free trade “pale in comparison to the impact of prospective financial concern” (page 225). The more insecure that people feel, the more they “hunker down” and one suspects that negative attitudes to trade in the USA are to a significant extent a reflection of a loss of national self-confidence and feelings of insecurity. In The Wolf at the Door, Michael Graetz and Ian Shapiro suggest that addressing this is the most important domestic challenge faced by America and it may be that, if it were adequately addressed, support for free trade would materially increase.

That said, Diana Mutz has done a great service to those who favour free trade by clarifying the causes of opposition to it. It is now up to others to work out how best to apply the implications of her research in influencing both politicians and public opinion.

“Winners and Losers” by Diana C. Mutz was published in 2021 by Princeton University Press (ISBN 978-0-691-20302-7). 275pp plus notes and bibliography.

Richard Godden is a Lawyer and has been a Partner with Linklaters for over 25 years during which time he has advised on a wide range of transactions and issues in various parts of the world.

Richard’s experience includes his time as Secretary at the UK Takeover Panel and a secondment to Linklaters’ Hong Kong office. He also served as Global Head of Client Sectors, responsible for Linklaters’ industry sector groups, and was a member of the Global Executive Committee.

It is common amongst politicians and economists to suggest that we should tax bad things and subsidise good things. It is on these grounds that, for example, we have sugar taxes and cigarette taxes. The justification for taxing “bads” becomes stronger if the ill effects are felt more widely through society and not just by the consumers.

Anybody looking at our tax system, with this principle in mind, might well conclude that our political class believes that families with two parents, and those families where one parent works part time or works entirely in the home bringing up children or looking after ageing parents, were a very bad thing. After all, we strongly penalise such arrangements in our tax and welfare systems.

In the United Kingdom, tax rates rise with incomes, but assessment for tax is based on individual and not on household or family income. This penalises families that have an uneven split of incomes between the adults – this will mainly apply where you have mothers undertaking caring responsibilities.

Take, for example, a couple where both adults earn £12,500 per annum. They will pay no income tax – literally, no income tax at all. If the same couple is a single-earner couple with one of the adults earning £25,000, they will pay income tax of £2,500. To have the same net income, the single-earner family would have to earn an extra £3,125. This blow is softened, marginally, by the married couples allowance, but this has little effect and it is quickly withdrawn as incomes rise. When you take account national insurance, things get worse. The dual-earner couple actually pays lower national insurance contributions than the single-earner couple, yet the dual earner couple will earn the right to two pensions rather than just one pension (though, in certain circumstances, the second adult in the single-earner couple can accrue state pension rights).

A sum of £3,125 is a lot of money to a couple with children on a low income. Earning this additional sum at the minimum wage would involve the main earner working an equivalent of eight extra weeks across the year. If this is a family with a stay-at-home mum, the father will hardly see his children.

It gets worse. When one of the earners within a couple reaches £50,000 per annum, child benefit is withdrawn. This policy almost seems to be designed to penalise single-earner families. More generally, the progressive nature of the tax system, together with some additional quirks, means that the tax system penalises single-earner families more and more as earnings rise. A single-earner family with three children earning £70,000 a year would pay £8,000 more in tax than a dual earner family with an even split of earnings. To make up this gap, the single-earner family would have to earn an extra £14,000. There are some circumstances in which the single-earner family would need to earn an extra £30,000 a year.

This situation cannot be justified. Governments measure inequality and poverty by looking at household income and not individual income. It would be absurd to regard an individual as poor if they do no paid work whilst being married to somebody earning £4million a year. So, if it is the resources of the family or household that matter for measuring inequality and poverty, why do we not tax families on the basis of the household income – or at least on the basis of the income of the two main adults, with all the rates and allowances being applied at that level? Two households with the same income should pay approximately the same amount of tax regardless of how that income is split between the couple.

Of course, it is clear in Judaeo-Christian thinking that the family is the basic cell of society. In Genesis 2:24 it is stated that “…a man leaves his father and mother and is united to his wife, and they become one flesh.” But secular philosophers such as F. A. Hayek thought that way too.

The UK tax system can be seen in a worse light if we consider how it interacts with the welfare system. A non-earning mother with a child will be given welfare benefits. If she marries, or even lives with, the father of that child she may lose those benefits if he has a job. And yet, there is no compensation in the tax system for the fact that his, possibly meagre, resources now have to be spread across three persons rather than just one.

Quite simply, our tax system penalises – in a substantial and explicit way – family formation and caring in the home. Families on similar incomes are treated far more harshly, simply by virtue of the fact that one parent might look after a parent or child. It does not have to be like this. The tax systems in Germany and France, treat families fairly. They tax families on the basis of family income. We should do the same.

Philip Booth is Professor of Finance, Public Policy and Ethics at St. Mary’s University, Twickenham

Philip Booth is Professor of Finance, Public Policy and Ethics at St. Mary’s University, Twickenham

The P&O debacle has become a touchstone for business ethics.

Few would like to be in the shoes of Peter Hebblethwaite, the Chief Executive, who admitted in oral evidence to a joint sessions of the Transport and the Business, Energy and Industrial Strategy Committees, that he had broken the law on consultation with trade unions. He argued that without this decision there was no future for the company and 3,000 rather than 800 job losses would result. The crews would be replaced with an agency model, with levels of pay above the internationally agreed levels for the model, but considerably below the UK minimum wage provisions. It was, he said, the only decision which could be made and he would do so again.

The basic facts

The facts on the ground are relatively straightforward.

There are some other disputed issues – for example, the requirement to give 30-45 days’ notice to relevant flag state authorities – for which there appears to be an exemption and whether or not the Secretary of State was informed, but there appears to be no disagreement on the main three points above.

The initial responses:

What options were available to P&O?

The company had lost, according to the CEO, an unsustainable amount of money, around £100m in the last year. What then were the options open to P&O?

There may have been other short-term options (property sales, loans) but in essence a company in the situation that faced P&O almost certainly has to reduce its wage bill, one way or another. Perhaps the chief executive was correct when he said that was no other decision he could make?

Nevertheless, if this is the case, why would you not follow the appropriate and required legal processes for achieving these redundancies? Why risk further damage to reputation by failing to do so?

Ethical observations

Ironically, the market may sort out both the economics and the ethics.

My real point is not to defend P&O, but that the rule of law provides remedy.

I am not sure that I like the fact that agency seafarers are paid such low wages. Indeed, for the government to take the lead in reforming the international maritime system would be a point of moral leadership. However, to arbitrarily introduce legislation affecting only British ports could destabilise the competitiveness of British ferry companies to the detriment of all their employees.

There are some signs that the government has accepted that legislation to achieve this is not possible under international agreements; indeed, arrangements agreed with international trades unions. There also appears to be some moves afoot to declare some or all P&O directors unfit with an investigation launched by the Insolvency Service into both criminal and civil liability.

I have no comment on whether the standards are met, but it is right that the company and its directors are held account for their actions. I do not support the manner in which these redundancies were handled at all. I believe workers should be properly and generously treated, their dignity respected and that they should be well-paid. P&O have done themselves serious business damage through the impact on their reputation, for which the directors are responsible.

However, we need far more care in discerning the real issues in this and similar disputes. The rush to judgement helps nobody and usually requires backtracking.

The market has an extraordinary way of filtering out bad business practice. The employees would probably be best advised to seek alternative employment and the unions advised to help them. But I also wonder whether the shareholders want a board of directors in place that causes such unnecessary reputational damage by failing to follow due process? The consequences are entirely commercial.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.

Some of the toughest and most complex challenges faced by businesses and corporations in today’s world involve ethics and morality. This is in part why the study of business ethics has now become central in MBA and other programmes. But the very complexity of these challenges, in an increasingly pluralized as well as globalized world, present a danger that companies lose sight of the big picture – failing to see the wood for the trees.

Lutge and Uhl seek to assist here by providing a comprehensive overview of the essential concepts of business ethics related to the economy as a whole. At the same time, they offer a wide-ranging analysis of the issues and tools that corporations need to be aware of as they consider the ethical and moral dimensions of their activities. So, this book – Business Ethics: An Economically Informed Perspective – is distinctive and helpful in the comprehensiveness of what it offers.

Lutge and Uhl are German-based scholars who evidently have deep knowledge in these very important areas – which cover a wide range of academic disciplines. The quality of their English writing is very good, and the book will be a valuable resource both for companies (especially medium-size and large companies), as well as individuals who have senior-level responsibility.

The authors sometimes refer to their book as a ‘textbook’. However, my impression is that is more of a comprehensive survey than a teaching book as such.

Chapter 1 sets the scene by discussing briefly the phenomenon of globalization. The authors argue that globalization poses a challenge to virtue ethics: “It is an enormous challenge to find some plausible common ground” for a meaningful ethical dialogue “if a common denominator of values does not exist” (pages 13-14). The authors propose that a more helpful approach is offered by order ethics: the focus here is more on rules than on values. “The key idea of order ethics is to look out for strategies on the level of rules that enable win-win solutions for all affected parties” (page 14). The authors return to this emphasis a number of times.

Chapter 2 provides a brief analysis of the relationship between ethics and economics. The authors interpret business ethics as ethics with an economic method. This links to the book’s subtitle: An Economically Informed Approach. Lutge and Uhl argue that, from the point of view of business ethics, “production and distribution should be recognized as interdependent and therefore only discussed simultaneously” (page 26). Similarly, “it is only in the interplay of ethical reflection and economically informed implementation that rules and institutions can be created that are resistant to exploitation and mutually beneficial” (page 31).

Chapter 3 surveys the development of business ethics thinking in the historical context of the distinction between premodern and modern companies. The authors include a brief survey of ethical teaching in the Bible and Christian thought, as well as Hinduism and Islam. They argue that the complexity of the 21st century world means that it is insufficient to have an ethics of behaviour: one must also think about the ‘ethics of conditions’, by which they mean the rules of competition (page 52). This chapter makes a strong case for the benefits of markets and competition. It also argues that business ethics can to some degree be regarded as a form of risk management. “Especially in an information society…it is in the company’s own interest not to ignore the moral dimension of its own actions” (page 37).

Chapter 4 is a more lengthy survey of key models and tools of business ethics and corporate ethics. It consists of three sections: the first looks at philosophical foundations and tools, such as deontology and consequentialism and contractual concepts (e.g., the work of Hobbes, Kant and Rawls). The second section focuses on economic and social-science foundations and tools, such as the rational actor, dilemma structures (e.g., the ‘Prisoners’ Dilemma’) and the concept of utility. These tools are applied to concepts of justice. The third section deals with psychological foundations and tools. Major subjects considered here include the social intuitionist model of moral judgment and the concept of bounded ethicality: a perhaps unfortunate piece of jargon which essentially refers to the study of how and why ethical decision-making can be inconsistent and thus problematic – both on the part of individuals and organizations.

It would be fair to say that the evident breadth and depth of Chapter 4 means that it is not easy reading. But this chapter does illustrate the usefulness of the book as a comprehensive survey, and thus a tool for reference and reflection.

Chapter 5 looks in depth at some of the challenges of the modern globalized world, and seeks to show how these impinge on business ethics. This chapter considers absolute poverty and relative poverty, and then evaluates the extent to which equality is a valid goal, in ethical terms. The authors’ overall approach is reflected in the following words: “It does not make sense to construct a fundamental trade-off between freedom and equality. Rather, there should be a search for win-win opportunities that improve all parts of society so that no group feels systematically left behind” (page 168).

Chapter 6 is the last and most comprehensive chapter in the book, and addresses a number of aspects of corporate ethics. In doing so, it pays due attention to the fact that companies are key players in the globalized world. Again, this book is seen to offer a very important survey of material and perspectives that are vital, especially for larger corporations. A number of case studies are provided (in this and other chapters) which help to highlight the practical nature of the challenges and ethical issues.

Chapter 6 provides a detailed analysis of compliance – as a minimum ethical requirement – including the limits of compliance. It then considers different perspectives on corporate responsibility, including the relationship between profit-maximization and ethical responsibility, and corporate ethics based on the role of ‘the honourable gentleman’ – this latter approach having been recently revived through, for example, the Harvard Business School: “As one of the world’s top management schools, it is providing a prominent stage for individualistic concepts and moral codes” based on honour (page 237). The authors are, however, sceptical and critical of this development: the question arises as to how such an approach “can be implemented in concrete terms in the context of value pluralism. Even if it were possible to agree on certain values – at least within a certain cultural sphere – there would be obvious disparities in the actual evaluation and respective weighting of particular actions” (page 238).

The authors argue, instead, that the complexity of the modern world “requires the implementation of ethical values in the form of rules and institutions” (page 239). However, it would seem that further thought is required here: unless there really is some given moral foundation for behaviour and conduct – such as that provided by the Christian faith – then any “implementation” of ethical values is ultimately lacking in foundation. Even though today’s world evidently exhibits some degree of moral pluralism – and hence relativism – it is still surely possible to draw people together to engage in meaningful conversation about what is right and just.

Chapter 6 concludes with a survey of concepts of corporate social responsibility, including the importance of guarding against reputational risk and loss that can arise if companies fail to act in line with ethical principles. Once again, this illustrates the usefulness of the book as a comprehensive reference, to help guide companies, and those who have senior responsibility, through the complexities that surround business ethics.

“Business Ethics: An Economically Informed Perspective” by Christopher Lutge and Matthias Uhl was published in 2021 by Oxford: Oxford University Press (ISBN 978-0-19-886477-6). 353pp.

Revd Dr Andy Hartropp is an economist, theologian and church minister. He has two PhDs, one in Economics and one in Christian Ethics. He lectured in financial economics for 5 years at Brunel University, west London. He also worked for a year with the Jubilee Centre in Cambridge, primarily leading a team doing research on families in debt. He trained at Oak Hill College, London, for ordained ministry in the Church of England. His (second) PhD was published as: What is Economic Justice? Biblical and secular perspectives contrasted (Carlisle: Paternoster, 2007). He has spent 13 years in parish ministry. He worked for eight years with the Oxford Centre for Mission Studies, where he was the Sundo Kim Research Tutor in Mission and Economics. In March 2016 he joined Waverley Abbey College as Director of Higher Education. He chairs the Ethics and Social Theology Group of the Tyndale Fellowship. He is married to Claire, and they live in Bicester, near Oxford.

Revd Dr Andy Hartropp is an economist, theologian and church minister. He has two PhDs, one in Economics and one in Christian Ethics. He lectured in financial economics for 5 years at Brunel University, west London. He also worked for a year with the Jubilee Centre in Cambridge, primarily leading a team doing research on families in debt. He trained at Oak Hill College, London, for ordained ministry in the Church of England. His (second) PhD was published as: What is Economic Justice? Biblical and secular perspectives contrasted (Carlisle: Paternoster, 2007). He has spent 13 years in parish ministry. He worked for eight years with the Oxford Centre for Mission Studies, where he was the Sundo Kim Research Tutor in Mission and Economics. In March 2016 he joined Waverley Abbey College as Director of Higher Education. He chairs the Ethics and Social Theology Group of the Tyndale Fellowship. He is married to Claire, and they live in Bicester, near Oxford.

CEME was delighted to co-host, in partnership with St Mary’s University and CCLA Investment Management, an in-person event on The Morality of Government Debt: insights from economics and Christian social thought. One economic consequence of the pandemic has been the accumulation of large amounts of public debt. This has huge ramifications and raises a wide a range of moral as well as economic questions.

Our panel of speakers were:

Terry Smith, chief executive of investment management company, Fundsmith, began his January 2022 letter to investors, ‘This is the twelfth annual letter to owners of the Fundsmith Equity Fund.’ Pretty routine stuff one might think.

Except.

Unilever was the second worse performing stock in the Fund. Smith did not hold back:

“Unilever seems to be labouring under the weight of a management which is obsessed with publicly displaying sustainability credentials at the expense of focusing on the fundamentals of the business. The most obvious manifestation of this is the public spat it has become embroiled in over the refusal to supply Ben & Jerry’s ice cream in the West Bank. However, we think there are far more ludicrous examples which illustrate the problem. A company which feels it has to define the purpose of Hellmann’s mayonnaise has in our view clearly lost the plot. The Hellmann’s brand has existed since 1913 so we would guess that by now consumers have figured out its purpose (spoiler alert — salads and sandwiches).”

Is Terry Smith correct?

There are a number of complexities in coming to a view on the matter, not least, that despite his tirade, Terry Smith goes on to say that the fund retains its holding in Unilever because despite the weak performance he believes that the company has strong brands and distribution and will triumph in the end. Smith also contradicts himself in his example. He complains about an obsession with sustainability but then gives an example of political lobbying.

Smith has strong point yet manages to mix up his responses.

Here at CEME we have recently undertaking an extensive poll / survey of various audiences including the general public, business leaders, church leaders and those of faith across a wide range of business, economic and ethical issues. Savanta ComRes polled across several audiences between 10th May 2021 – 5th August 2021 with the following samples:

The full analysis of this survey will be published in the next few weeks but there is one aspect of these findings that reveal exactly why Smith is both right and wrong at the same time (at least in the eyes of the public at large).

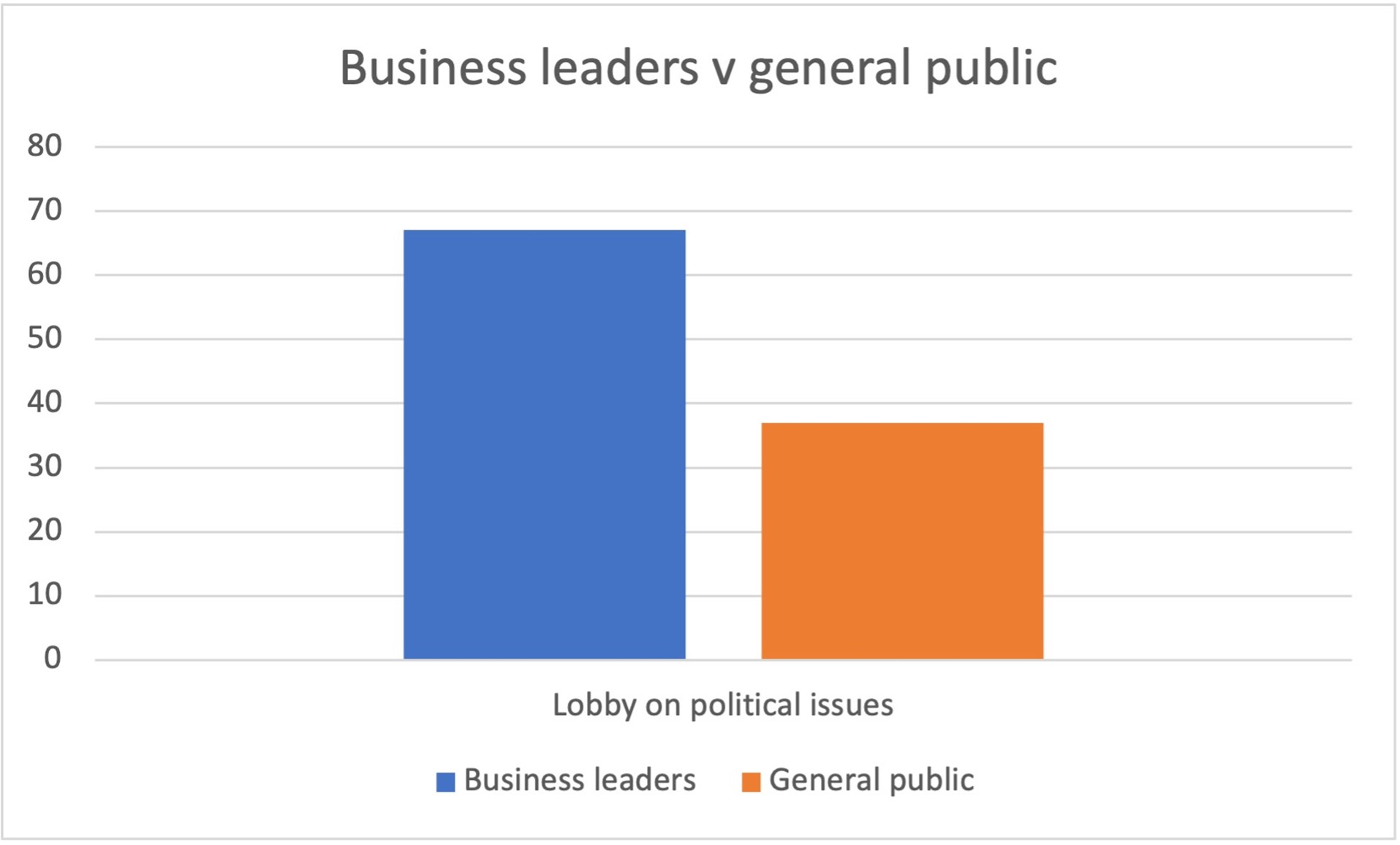

The general public do not want political campaigning and lobbying by business.

In this case Terry Smith’s point about the purpose of Hellman’s is bang on the nail. The public want mayonnaise on their sandwiches and salads, as he puts it. The public want high quality goods and services – whether the mayonnaise or tasty ice cream from Ben and Jerry’s

Furthermore, Smith is onto something when he is talking about the management. The disparity of the views of business leaders compared to the general public is extraordinary. Approximately 67% of business leaders support lobbying or advocacy on political issues by business. Among the general public this drops to just 38% as shown in the chart below.

Amongst the over 55s support for political lobbying fell to a mere 28%.

This is one example of business losing sight of its basic purposes – the public simply want the delivery of quality goods and services. Our survey revealed several more, to be revealed when we publish the full analysis!

The position is even more interesting when we considered the response by business leaders according to size of company. For those in companies with more than 1,000 employees the percentage of business leaders supporting political advocacy and lobbying rose to an astonishing 79%.

What on earth do big businesses think they are doing?

This is also an example of how an elite becomes alienated from the wider community and public. Business leaders seem to have lost sight of their actual job in the market. Please, please, just deliver the mayo and the ice cream!

At this point we might conclude that Terry Smith is right and business must cease its lobbying on politics, environment and sustainability. Not quite.

The public distinguish between political and environmental activism

One of the fascinating things about this research is a clear distinction in the public mind between political lobbying and environmental concerns. The public are with Terry on the politics, but not on the environment.

In overall terms the results show substantial support for business concern for the environment and action on climate change. The results in these areas were as follows:

Why the disparity?

There are two reasons why this might be so.

Terry Smith then was partially right. Too much obsession with social purpose and politics is not what the general public want and alienates business from the very people it is intended to serve (in the sense that if business does not supply the goods and services in the market at a price determined by supply and demand, there will be no profits, not for shareholders or anybody else). As Oscar Williams-Grut, City editor of the Evening Standard put it, “sometimes mayonnaise is just mayonnaise”.

Yet, Terry also missed a point. By linking his message about politics with the environment he failed to notice the sea change in opinion which has taken place. Drop the politics, but the public do want business to have a wider concern, not least in terms of stewardship of the environment for the benefit of all.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.

The Wealth of Religions is an unusual book. It is subtitled, “The Political Economy of Believing and Belonging” and its authors, one an economist and the other a moral philosopher (who, as it happens, are married to one another), seek to present a multidisciplinary approach to issues at the interface between religion and economics. They say that they “are interested in the economic costs and benefits of holding certain religious beliefs and the influence of those beliefs on behavior” (page 4) and that their central approach “is the application of economic and political principles to the study of religions across countries and over time” (page 9).

The book is divided into two sections: the first looks at the interplay between religion and economic growth whilst the second deals with issues associated with the connection between religion and political economy. The first takes as its starting point Max Weber’s famous argument relating to the protestant work ethic, although the authors’ arguments are not by any means identical to those of Weber; the second is particularly indebted to what the authors regard as Adam Smith’s ingenuity in applying his market model to religious goods and services “as if they were analogous to brands of toothpaste” (page 106).

The book has severe limitations. It is based on short articles published over the past couple of decades and it fails to disguise this; despite only being a short book (172 pages), there is a significant amount of repetition and there is an element of miscellany about its contents, particularly in the second section. Some of the material is frustratingly general (e.g. the section relating to the impact of religion on economic growth) whilst some of it is so specific that it will not interest many readers (e.g. the 23 page chapter relating to beatifications and canonisations by the last three popes). The result is that the book lacks an overarching argument or sense of direction, and it is unlikely that many readers will be interested in all of it.

Nonetheless, the book addresses interesting and thought provoking questions and the diversity of its material has an upside: any reader who is interested in either the interaction between economics and religion or the way in which economic concepts may have an impact upon organised religion will find something engaging in it.

This mixture of the unsatisfactory and the engaging is exemplified by the second chapter, which explores how the economy and the regulatory system influence religion in society. John Wesley famously observed that, as people become richer, they become less devout and the authors wish to test this observation (the so-called “secularisation hypothesis”). Many readers will be impatient that it takes the authors 12 pages to come to what they will regard as a blindingly obvious conclusion: “we find a strong negative effect on all measures of religiosity from higher economic development” (page 28). However, the authors also discuss some less obvious issues and reach some interesting conclusions including, contrary to the views (and perhaps hopes) of some vociferous atheists, “there is no evidence in cross-country data that more years of education reduce religiosity” (page 31).

The third chapter (relating to the impact of religion upon economic growth) is likewise a mixture of the disappointingly superficial and the tantalisingly interesting. The Weber thesis is explained and various religious views of salvation surveyed in a mere eight pages, which include some highly contentious statements (e.g. the assertion that Calvin did not believe in the possibility of assurance of salvation, which is justified by a statement in his Institutes that is taken out of context and fails to notice that, in the very same section of the Institutes, Calvin states that faith is “a firm and sure knowledge of the divine favour toward us, founded on the truth of a free promising Christ, and revealed to our minds, and sealed on our hearts, by the Holy Spirit”). However, from this unpromising start, the authors go on to discuss their own analysis of detailed international data and come up with some interesting conclusions. For example, they show that this data suggests that belief in heaven and hell (and particularly the latter) is positively correlated to economic growth but belief in God or a general posture of being religious is not. Furthermore, for any given belief in hell, an increase in monthly church attendance appears to lead to a decline in economic growth and, to put the matter the other way up, for any given church attendance, an increase in belief in hell leads to an increase in economic growth. The authors also provide a brief survey of various pieces of academic research that suggest that the oft-repeated suggestions that the positive impact of Protestantism is either associated with “belonging” or to Protestantism’s promotion of human capital via education are misconceived.

Of course, Weber’s thesis related to the impact of Christianity and, specifically Protestantism, in Europe and any globally applicable theories relating to the impact of religion on economic growth (or vice versa) need to take account of the impact of other religions. The authors recognise this issue and, to some extent, seek to address it, particularly in chapter 4, which relates to Islam and economic growth. However, these parts of the book are again superficial. The entire sweep of Islamic economic history is dealt with in 10 pages and the authors fail to provide convincing evidence of the impact of Islam on the economy; other major religions are scarcely considered. The result is that a number of major questions of significant importance in the modern world are not addressed at all (e.g. the impact of Hinduism on the economic development of India).

More generally, the application of economic concepts to organised religion, whilst potentially thought provoking, is contentious and may even be offensive to some people. For example, one does not need to be a Roman Catholic to raise eyebrows at the statement that “our assessment is that the increased numbers and geographical spread of persons named as blessed and the targeting of popular ex-Popes are clever innovations aimed at raising the enthusiasm of Catholics” (page 154); and one does not need to be a Buddhist to feel somewhat uneasy when reading the title of chapter 6: “Religious Clubs, Terrorist Organisations, and Tibetan Buddhism”. Furthermore, many Christians will consider that the “supplier and consumer” model of religion presented by the authors is indicative of precisely what is wrong with much Christianity today rather than an indication of fundamental features of its success or failure.

That said, despite all of its inadequacies, and having regard to its relative brevity, The Wealth of Religions is worth reading and, having read it, some readers may well find that there is plenty to interest them in the bibliography, which reflects the cross disciplinary nature of the book itself.

“The Wealth of Religions” by Rachel M. McCleary and Robert J. Barro was published in 2019 by Princeton University Press (ISBN – 13:9780619217109). 172pp.

Richard Godden is a Lawyer and has been a Partner with Linklaters for over 25 years during which time he has advised on a wide range of transactions and issues in various parts of the world.

Richard’s experience includes his time as Secretary at the UK Takeover Panel and a secondment to Linklaters’ Hong Kong office. He also served as Global Head of Client Sectors, responsible for Linklaters’ industry sector groups, and was a member of the Global Executive Committee.

Charles Boix is Professor of Politics and Public Affairs at Princeton University. His primary research interests are in political economy and comparative politics, with a particular emphasis on empirical democratic theory. Previous notable publications include Political Parties, Growth and Equality (Cambridge University Press, 1998), Democracy and Redistribution (Cambridge University Press, 2003), and Political Order and Inequality (Cambridge University Press, 2015).

In Democratic Capitalism at a Crossroads Charles Boix seeks to explore both the historical chapters of democratic free-market tensions and current issues facing capitalism within western democracies. The author divides the narrative into three main eras: 19th century Manchester capitalism, 20th century Detroit capitalism, and the current 21st century Silicon Valley-based model of capitalism. The final chapters consider the implications of these forms of capitalism on the future workforce, in particular with respect to automation, the rate of technological change, income distribution and politics (or the role of government more broadly).

Charles Boix’s thesis is that, “the consequences of today’s technological changes […] are not set in stone. They will work their way into the economy through their direct (although, at this point, still uncertain) impact on the demand for different types of labour and on the cost and ownership of capital. Yet they will also depend on the institutional and political strategies we follow in response to those technological transformations” (page 3).

The book is well-written and comprehensively researched. The author does a commendable job of avoiding the clichés that often surround the topic of technology and maintains both nuance and a satisfactory degree of objectivity. We will touch upon some of the more intriguing points made throughout the book.

Chapters 1-3 explore the impact of technology on society and politics from a historical perspective. Chapter 2 dedicates a fair amount of attention (and rightly so), to the first industrial revolution. Boix points out that automatization brought by a new class of comparatively poorly skilled labour that replaced “…an old class of artisans and highly skilled operators” (page 57). In 20th Century capitalism however, the advent of technology (and automisation more specifically), led to a further replacement of low skilled workers with semi-skilled workers – albeit in much lower numbers. This new workforce of semi-skilled labour was needed to oversee, maintain, and repair the machinery in operation. Yet perhaps the most important consequence of the process of automisation was the arrival of “… new layers of white-collar, relatively well-paid jobs – from accounting departments to car dealerships” (page 59).

This in effect resulted in a new form of Corporatism whereby the relationship between employees, trade unions and the employers are far more interwoven than before. An interesting point is made in chapter 3 whereby the continual development of a company’s human capital became a vested interest for the company itself. Henry Ford for instance invested heavily in the education of his workforce. He established the Ford English School to teach English to recently arrived immigrants and he even established a “…Sociological Department, with about two hundred employees, to ensure that the family lives and overall behaviour of his factory workers did not deviate from a clear set of norms such as thriftiness, continence, and basic hygiene” (page 78).

Chapters 4-6 move the conversation to the contemporary debate around technology, artificial intelligence (AI), and its impact on the labour markets and consequently, on democracy itself. Charles Boix rightly points out the difference between simple AI and machine learning. The key form of impact here is that while computers/AI displaced routinable jobs at a large scale, they have “…hardly replaced nonroutine jobs” (page 103). Though this may be changing with machine learning.

Boix acknowledges in Chapter 6 that, ultimately, we cannot predict the impact of technological change or indeed “…depict the society it will give birth to…” (page 180). Therefore, any future policy responses must be made in a piecemeal fashion (ibid.). The chapter concludes the book with a few tentative proposals for reform. Rather unexpectedly, Universal Basic Income (UBI) is presented as one such proposal – yet the arguments made against UBI seem more convincing than those in favour. For instance, the author claims that UBI has two main advantages: “First, it may free individuals from routine, repetitive tasks, allowing them to engage in more creative and inventive professional paths. Second, it should reduce poverty and arguably, equalise conditions” (page 206). Perhaps the keywords here are ‘may’ and ‘should’ – one cannot help but feel that this is mere wishful thinking.

On the challenges of UBI, Boix acknowledges a rather lengthy list: UBI cannot be tailored to individual needs, it distorts the incentives that people have to work, it may keep the pre-existing structure of inequality in place, it reduces the need for schooling, it enables firms to offer lower wages, it affects the inner motivations and ambitions of youngsters, it can create antagonism between those that are earning against those that are not (pages 207-208). We don’t have space to go into further detail here, and surely each reader will make up their own mind – but it is a strange and slightly disappointing end to an otherwise interesting book.

In summary, Democratic Capitalism at a Crossroads is an engaging read about the impact of technological change on the transformation of labour markets, society and indeed, democratic systems themselves. It is accessible to the educated reader and while some might take issue with certain sections of the book, the author does a laudable job of curtailing his more subjective opinions by also presenting the counterarguments. One result is that some readers may find the counterarguments more compelling than the main arguments themselves (UBI is a case in point). This might not necessarily be a bad thing. The book is a recommended read to those looking to expand their knowledge of the intersection between technology, the economy, and democracy.

“Democratic Capitalism at the Crossroads” by Carles Boix was first published in 2021 by Princeton University Press, ISBN: 9780691216898, 272pp.

Andrei E. Rogobete is the Associate Director of the Centre for Enterprise, Markets & Ethics. For more information about Andrei please click here.

The Centre for Enterprise, Markets and Ethics (CEME) is delighted to announce the publication of Government Debt: A Neglected Theme of Catholic Social Teaching by Philip Booth, Kaetana Numa, Stephen Nakrosis and Richard Turnbull.

Government debt in developed countries has risen sharply in recent decades, yet Catholic social teaching — which has engaged extensively with sovereign debt in the developing world — has paid surprisingly little attention to its moral implications closer to home. This essay seeks to fill that gap.

The authors begin by charting the growth of government debt across several major economies, noting that peacetime reductions have become increasingly rare and that “implicit” liabilities — unfunded pension and healthcare promises — may dwarf the official figures. They examine the various reasons governments accumulate debt, from wartime necessity and counter-cyclical spending to the perverse incentives facing democratic electorates, who may prefer to consume today at the expense of future taxpayers.

The central moral argument turns on intergenerational justice. Drawing on the creation mandates of Genesis, the scriptural emphasis on stewardship and wealth creation, and Catholic principles of distributive justice, the authors contend that systematically burdening future generations with debt — or with unfunded social-insurance obligations — is difficult to reconcile with the dignity owed to all persons across time. They supplement this with perspectives from the wider Protestant tradition, including Calvin, Kuyper and Chalmers, all of whom point towards a limited but purposeful role for the state and a strong presumption against excessive public indebtedness.

Historical case studies — from Bourbon France and nineteenth-century Egypt to interwar Germany, Argentina and the eurozone crisis — illustrate how high debt can impair democratic accountability, provoke inflation and default, deepen poverty and undermine the very functions of government that Catholic social teaching regards as essential. The authors conclude that excessive government debt sits uneasily with Christian teaching and deserves far greater attention within Catholic social thought.

A PDF copy can be found here. A hardcopy of the publication can be ordered by contacting CEME’s offices at office@theceme.org

60 per cent of business leaders and, indeed, 75 per cent of leaders in larger businesses, think profit is incompatible with a society in which people are happy. Incompatible. The figure for the general public is just 37 per cent. Similar percentages of business leaders think business should be taxed more and executives are paid too much.

According to British Religion in Numbers around 2.5 million were attending church in 2015, a considerable number. A mere 30 per cent of church leaders think that employers care about their employees, 75 per cent think business leaders are paid too much, and only 30 per cent trust multi-national enterprises. For the committed flock these results are 56 per cent, 65 per cent and 73 per cent respectively, some enormous differences. The numbers don’t improve when we consider society and taxation. There are surprisingly high levels of support for high taxation as a way of achieving a fairer society, Universal Basic Income, reliance on government grants to support entrepreneurs amongst both business leaders and church leaders.

In essence our national establishment and elites have lost their conviction in the market economy and power of business for economic well-being. They have lost confidence in the nation as a place to do business, the role of profit, competition, incentive and innovation. They are, however, out of touch, with the general public and with the committed in the pews.

This is the result of polling conducted for the Centre for Enterprise, Markets and Ethics. Savanta ComRes polled six audiences between 10th May 2021 and 5th August 2021 to secure their findings: the general public, regular churchgoers, business leaders, Muslim and Jewish people, and Church leaders. They also conducted in-depth interviews between 10th May 2021 and 5th August 2021 with ten Anglican and Catholic bishops. The total sample size was just short of 3,500 people.

The business community seem less supportive of the market than the general public on just about every metric. Perhaps business leaders are actually out of touch with the public, the people who actually buy the goods and services they produce?

They certainly are on the headline topics. 60 per cent of business leaders may think profit is not compatible with a society in which people are happy, but only 37 per cent of the general public agree. There are also gaps on corporate tax, executive pay, political campaigning and even pay ratios (public less interested than business leaders). The results also show that those who preach to the flock hold opinions on business and enterprise, tax and society far removed from those who listen in the pews, if they are still listening. Perhaps the faithful are more in touch with God?

According to the polling 51 per cent of church leaders viewed higher taxation as a better way of achieving a fairer society than lower taxation. This is probably predictable as nobody really seems to make the case for a low-tax economy today. Perhaps the case needs to be made afresh? There would certainly be an open door among the faithful; only 34 per cent of weekly churchgoers had the same rose-tinted view of high taxation as the clergy.

Committed churchgoers – defined as those who attend weekly – have a considerably more positive view of business and the market economy than those who lead them and teach them on matters ranging from trusting multinational and employers caring about employees.

Disturbingly there seems to be among clergy a loss of confidence not only in many aspects of the market economy but also in the nation itself. In response to the question whether Britain was an attractive place to do business only 46 per cent of the church leaders thought so, compared to 66 per cent of the congregation members.

What has led to our national elites losing such confidence in the power of enterprise and the market? What has happened to our business leadership that might lead to this extraordinary state of affairs?

The idea of a competitive market with reward and incentive for risk and innovation producing the goods and services which the public demand has drifted onto the back-burner, accompanied by increasing reliance on government. But if those who are at the heart of enterprise don’t really believe in what they are doing the implications for both the economy and society are enormous. And those who preach to millions of the flock Sunday by Sunday a message is being preached that is not believed by most of its recipients.

What lessons can we learn?

First, business should focus on business. The idea of the business enterprise is to produce goods and services in a competitive market. The high ideals of quality, innovation and new ideas lie at the heart of an enterprise-focussed economy. Perhaps this type of innovation will be what contributes to solving environmental and climate challenges rather than big government?

Second, we must again advocate for a market economy, with thriving businesses and a flourishing society. We need to restore confidence in the market and enterprise, promote business independence and less reliance on the role of government and high taxation. And we need to restore confidence in Britain as a place for business.

Third, make no assumptions. We cannot assume that the case for the market is a given, not even in the business community. We need more business advocates. The case must be made again for a market economy, amongst all-ages, for if we do not, the idea of a high-wage, low tax economy will be for the birds by default.

An effective market economy requires thriving businesses and flourishing participants in the market. Profit is not a dirty word, rather it is an essential component of economic well-being. Competition is good. We must promote business independence, less reliance on government and the growth and innovation that flows from lower, not higher levels of taxation. We need to promote Britain as a great place for business and learn the lessons before we lose the case for the market without noticing. The public understand that need. So too do the flock.

This was first published on Comment Central.

Dr Richard Turnbull is the Director of the Centre for Enterprise, Markets & Ethics (CEME). For more information about Richard please click here.