Chapter 4

Capitalism’s Great Divide: The Two Sides of Self-Interest

Tim Weinhold

Adam Smith probably tops history’s list of influential teachers with the most followers who largely misunderstood their teacher’s message. As we all know, Smith is widely viewed as the father of capitalism, based on his 1776 book, The Wealth of Nations. Smith and his book remain hugely influential to this day.

His principal thesis was that individuals – and enterprises and countries – should focus their productive activities on that which they do best, and then, via a free market, trade their specialised outputs for the goods and services produced by others. He argued that this combination of specialised production, with supply-and-demand-based free-market trading, most efficiently allocates productive resources and, as a result, maximises overall wealth creation. As well, it (generally) maximises utility for all participants; that is, everyone is better off.

Smith’s core contention, therefore, is that the market’s ‘invisible hand’ transforms self-interested production and trading behaviours into outcomes of maximum economic and social benefit. This has provided the foundational rationale for business and free markets – in other words for capitalism itself – ever since. Much of this is summed up in the book’s most famous sentence: ‘It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their regard to their own self-interest.’

A malignant misunderstanding

Arguably no other single sentence has ever been so thoroughly misunderstood, by so many people, to such disastrous effect. In fact this misunderstanding goes to the heart of why so many are now so critical of contemporary capitalism. More specifically, it explains why the rewards of late-twentieth and twenty-first-century capitalism have flowed increasingly to the wealthy, while the fortunes of much of the (Western) middle class, working class and poor have deteriorated.

The misunderstanding arises from a failure to recognise that, morally and practically, there are two very different kinds of self-interested behaviour. One occurs when an individual – or enterprise – acts for their own benefit at the expense of someone else. We generally describe such behaviour as selfish and predatory. Fortunately, there is a quite different sort of self-interested behaviour – where someone achieves a favourable outcome for themselves and for the other individual(s) affected by their action.

Though both behaviours are self-interested, their effects are poles apart. The first unilaterally imposes costs on someone else, making them worse off; that is, they are harmed. The second, by contrast, benefits not only the one taking action but the other party as well.

It is not surprising, then, that from our toddler years on we experience being on the receiving end of these two behaviours very differently. Reflect back, for example, on your own toddlerhood. Suppose you had been playing with a favourite toy and your older sibling came by and snatched it away saying, ‘I want to play with this now!’ Not very hard to recall how you felt, right? A terrible injustice has been perpetrated! Call in the authorities (Mom or Dad)! Such a grave wrong, such a violation of all that is just and proper, must be put right – NOW!

Suppose, though, that your sibling had said, ‘I’d like to play with your toy now, so how about if I let you play with my super-duper new toy?’ Provided that the new toy in question really was super-duper, you probably would have been quite happy to accede. In both cases, the result for your sibling was the same – they got to play with the toy they wanted. But the respective outcomes for you are quite distinct: in one scenario you were disadvantaged (harmed); in the other you were made better off (helped).

If even a toddler instinctively understands the watershed difference between these two versions of self-interest, why, we might ask, has it proved so difficult for adults – specifically economists, business people, business academics, political commentators and the like – similarly to understand that difference when it comes to the way business, and capitalism, are meant to work?

Devotees in the dark

Yet a great many of Adam Smith’s devotees find themselves unable to grasp that distinction. Over and over they evidence a belief that, effectively, Smith’s most famous sentence reads, ‘It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their selfishness.’ They believe that Smith was claiming for free markets and capitalism something quite extraordinary: that they magically transmute the lead of selfishness and exploitation into the gold of maximised benefit for individuals and society. This is nonsense and delusion.

And yet we find the Harvard economist Edward L. Glaeser declaring in The New York Times:

Two hundred and thirty years ago, Adam Smith made the case for selfishness when he wrote that ‘it is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own self-interest.’[1]

Or we read comments like this one, attributed to one of the two most influential economists of the twentieth century, John Maynard Keynes: ‘Capitalism is the extraordinary belief that the nastiest of men for the nastiest of motives will somehow work for the benefit of all.’[2] Keynes may simply have been paraphrasing an earlier quotation from a close colleague, E. A. G. Robinson, who wrote in his book Monopoly: ‘The great merit of the capitalist system, it has been said, is that it succeeds in using the nastiest motives of nasty people for the ultimate benefit of society.’[3]

Of course, no one has done more to associate capitalism with selfishness – and its close corollary, greed – than Ayn Rand. Then again, in her full-on defence of selfishness and greed, maybe she meant something different from what we imagine. Rand acknowledged, for instance, in the introduction to her book The Virtue of Selfishness, that she was using the term ‘selfishness’ to mean, more precisely, ‘concern with one’s own interests’.[4] Hmmm.

Along similar lines, consider this defence of greed from the other most influential economist of the twentieth century, Milton Friedman:

Well first of all, tell me: Is there some society you know that doesn’t run on greed? You think Russia doesn’t run on greed? You think China doesn’t run on greed? What is greed? Of course, none of us are greedy, it’s only the other fellow who’s greedy. The world runs on individuals pursuing their separate interests … there is no alternative way so far discovered of improving the lot of the ordinary people that can hold a candle to the productive activities that are unleashed by the free-enterprise system.[5]

If smart, prominent commentators like these are going to treat ‘selfishness’ and ‘greed’ as synonyms for ‘self-interest’, no wonder so many devotees imagine Adam Smith claimed the market’s beneficent hand turns selfishness and greed into social and economic blessing. This has done great harm. In particular it has caused a great many business people to believe that selfish, exploitative behaviour, though toxic in every other arena of life, is somehow magically beneficial when practised in business.

Impact, not motivation

But failing to distinguish the words ‘selfishness’ and ‘greed’ from ‘self-interest’, as sloppy and unhelpful as that may be, is not our real problem. Rather, the words themselves focus our attention in the wrong direction – towards the character and motivation of the actor. As a result, they keep us from recognising what truly differentiates good from bad and moral from immoral behaviour.

Let’s revisit for a moment our hypothetical scenario from your toddlerhood. When your sibling wanted your toy, your response had nothing to do with his or her motivations or character. If your sibling’s behaviour injured you – made you worse off – then you knew you had been mistreated and a wrong perpetrated. Period. If, instead, their action left you better off, you were happy to approve their behaviour – whether or not they were motivated by self-interest, selfishness or greed.

You knew your sibling’s conduct was wrong, or not, entirely based on the effect it imposed on you. Which means that, even as a toddler, you were thinking clearly as to what actually differentiates behaviours that are good from bad, right from wrong, moral from immoral; and that you were already thinking clearly about how we should assess good versus bad business conduct, and the difference between moral versus immoral versions of capitalism.

The golden rule

Of course, there’s more here than the justice instincts of toddlers. Throughout human history – across religions, across civilisations, even now in our post-religious Western secularism – one principle has always provided the bedrock foundation for human morality: the golden rule – ‘Treat others as you yourself wish to be treated’; or in its alternative rendering – ‘Love your neighbour as yourself.’ Notably, this cornerstone moral principle zeroes in on our actions – how we actually treat others – not our motivations.

Just as notably, the golden rule envisages a behavioural landscape comprised of not two but three impact categories – two of which meet the golden rule test. One such behaviour/outcome occurs when an individual – or enterprise – chooses to do good for someone else to their own detriment. We typically refer to such behaviour as altruism or selflessness. More precisely, though, we can label this ‘lose–win’ behaviour. The one taking action is disadvantaged for the sake of benefiting another.

Most of us have a tenuous relationship with selflessness. We acknowledge its moral attractiveness yet practise it infrequently. There are exceptions, of course. Many parents exhibit a great deal of lose–win behaviour towards their children. Good soldiers in combat may do so as well. And good spouses. Nevertheless, selflessness seems more the province of saints like Mother Teresa than us ordinary mortals. Across the landscape of human behaviour it is decidedly more the exception than the rule.

Fortunately there is another behaviour/outcome that also fulfils the golden rule. Win–win behaviour, as noted earlier, occurs when someone’s conduct brings about a beneficial outcome for themselves and for the other individual(s) affected by their action. Such behaviour is almost always motivated by self-interest. Yet it entirely meets the ‘Love your neighbour as yourself’ moral test.

Selflessness, therefore, is not the only way to keep the golden rule. Self-interested actions also meet the test for good and moral behaviour — provided they don’t come at the expense of others. It’s only when self-interest crosses over from win–win behaviour into win–lose territory that it violates the golden rule and becomes what most of us call selfishness (Ayn Rand and certain economists notwithstanding). A simple summary diagram should prove helpful (see Figure 1).

A great deal of what passes for moral commentary, at least as it relates to business and economics, assumes the important moral watershed is between selflessness and selfishness (or self-interest) – as if the foundational injunction is to ‘Love others rather (or more) than yourself.’ This both misunderstands the golden rule and misses the moral divide of real consequence.[6]

In fact the line of first-order significance is that between win–win mutuality and win–lose selfishness. It is here that we find the precise divide between what is moral and immoral, the exact boundary between right and wrong. It is also the difference between good and bad outcomes or, more broadly, between blessing and blight. More prosaically it is the difference between the merchant who makes money by providing a beneficial product and the mugger who takes money at knifepoint – or the loan shark (or payday loan company) who does so via extortionate interest. One practises a morally commendable self-interest, while the others’ behaviour is morally reprehensible.

Smith’s moral understanding of self-interest

As a moral philosopher, Adam Smith understood this distinction clearly, even if many of his followers do not. In his book The Big Three in Economics: Adam Smith, Karl Marx, and John Maynard Keynes, the prolific economics author Mark Skousen describes Smith’s fundamentally moral understanding of self-interest:

Smith recognized that people are motivated by self-interest. It is natural to look out for one’s self and one’s family above all interests, and to reject this would be to deny human nature. Yet at the same time, Smith did not condone greed or selfishness. For Adam Smith, greed and selfishness are vices.[7]

Skousen elaborates Smith’s morally circumscribed view of self-interest in a piece for the Foundation for Economic Education:

[Smith] wrote eloquently of the public benefits of pursuing one’s private self-interest, but he was no apologist for unbridled greed. Smith disapproved of private gain if it meant defrauding or deceiving someone in business. To quote Smith: ‘But man has almost constant occasion for the help of his brethren … He will be more likely to prevail if he can interest their self-love in his favour … Give me that which I want, and you shall have this which you want, is the meaning of every such offer.’ In other words, all legitimate exchanges must benefit both the buyer and the seller, not one at the expense of the other.

Smith’s model of natural liberty reflects this essential attribute: ‘Every man, as long as he does not violate the laws of justice, is left perfectly free to pursue his own interest his own way, and to bring both his industry and capital into competition with those of any other man, or order of men.’[8]

All of which makes especially compelling Smith’s pithy, emphatic statement of what we might call the ‘foundational justice dictate’ in his earlier (1759) masterwork, The Theory of Moral Sentiments: ‘There can be no proper motive for hurting our neighbour.’[9] It would be hard to misinterpret that.

The bottom line is this: Adam Smith, the father and foremost apologist for self-interested capitalism, nevertheless saw a bold bright line between actions that benefit both us and our neighbour versus those that help us but harm our neighbour. He recognised that a self-interested win–win mutuality was essential to business success and the creation of wealth, yet never countenanced win–lose selfishness and predation. He knew that taking advantage of others for one’s own benefit is both deplorable and dangerous. Smith understood clearly (along with virtually every other moral thinker throughout history) that such predatory behaviour undermines the very foundation of human society – and deserves to be roundly condemned by all.

Why this matters

This is consequential for three key reasons:

- Many CEOs countenance win–lose plunder and predation in their business models out of the mistaken belief that the father of capitalism claimed markets transform business selfishness into social well-being. Adam Smith did no such thing. Smith offers business leaders no magical-thinking smokescreen for practices that harm or exploit their stakeholders.

- The distinction between helpful versus harmful versions of self-interest points us insightfully towards what has gone wrong in our contemporary – late-twentieth and twenty-first-century American public company – expression of capitalism. We will turn to this subject in a moment.

- Even more importantly, it points us towards a reformed – really a restored – version of capitalism that does, indeed, ‘work for everyone’. Notably, it does so without asking business people to become particularly high-minded or altruistic. This reformed capitalism requires no abandonment of self-interest for the sake of ‘the greater good’, nor a forswearing of profit. It simply acknowledges that there are necessary limits to both. We will take up this subject in due course.

The turn towards selfishness

During the middle portion of the twentieth century, American business was the envy of the world. American corporations were the pre-eminent global leaders in virtually every industry. And the prevailing view among CEOs and business academics was that the purpose of a corporation was to create value for several different constituencies, more or less in this rank order: customers, employees, host communities, society and shareholders. In practice this meant companies generally aimed at win–win outcomes vis-à-vis their various stakeholders.

But starting in the 1970s, American business embraced an entirely different conception, a view that the pre-eminent purpose of a corporation is to maximise the wealth of its owners.[10] This view, labelled ‘shareholder value maximisation’ (SVM), has been the prevailing consensus ever since.

This watershed reconception of business purpose was first advanced by Milton Friedman in his famous 1970 opinion piece in The New York Times Magazine entitled, ‘The Social Responsibility of Business is to Increase its Profits’.[11] Then in 1976 two business academics, Michael Jensen and William Meckling, published ‘Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure’.[12] This hugely influential article argued for giving CEOs substantial grants of stock, or stock options, to better ensure their energies were pointedly focused on behalf of shareholders.

But it was in the 1980s when business people themselves embraced in a big way this new understanding of corporate purpose. They were especially influenced by Jack Welch’s 1981 speech, ‘Growing Fast in a Slow Economy’, in which he made clear that, henceforth, General Electric’s primary objective would be to return maximum value to shareholders.[13] This conception of corporate purpose has reigned supreme in America ever since. (It got considerable, but less, traction in other English-speaking countries, and relatively little in Europe.)

In practice, SVM has translated into a rigorous focus on maximising short-term profits. But maximising one outcome necessarily means sacrificing others. So when profits conflict with creating value for customers (or with the good of employees, suppliers, host communities or even society as a whole), SVM dictates that profits prevail.

In fact this understates the distorting effect of SVM. Once corporate purpose is defined in terms of immediate maximised wealth for shareholders, the priority job of senior management becomes channelling every dollar possible away from employees, suppliers, communities, society, even away from research and development for future growth – all for the sake of a fattened bottom line this quarter or next. SVM represents, therefore, a giant turn towards selfishness, towards advantaging business owners – senior management owners in particular – at the expense of everyone else.[14] Consequently a great many businesses have moved squarely into the win–lose, plunder and predation end of the moral landscape.

The effects have been severe. Rather than a last resort, layoffs are now a go-to choice to boost near-term profits. Pension plans have all but disappeared. For many retail workers, so too have predictable hours and incomes. More and more health care cost has been pushed from employers to employees. At a more foundational level, the ‘gig economy’ threatens to undo the entire landscape of worker protections, blithely turning employees into contractors with virtually no rights or security. And maybe most significantly, the share of economic output flowing to profits (shareholders) is at an all-time high, while the proportion flowing to workers has never been smaller (see Figure 2).[15]

Of course, corporate win–lose predations are hardly restricted to employees. Anti-customer corporate scandals – GM’s ignition switch, VW’s emissions cheating, Wells Fargo’s bogus accounts, Wall Street’s seemingly endless stream of malfeasance – have become commonplace. So has corporate tax avoidance, including through domicile inversions and aggressive use of tax havens.

And what about unilaterally pushing business costs onto taxpayers? As a rather notable instance, American taxpayers spend in the vicinity of $8 billion a year providing poverty assistance benefits to Walmart workers[16] – despite the company topping the 2016 Fortune Global 500 with revenues of $482 billion. And, of course, there’s this egregious example of misbehaviour: less than a decade ago the greed and recklessness of our largest financial institutions came within a hairsbreadth of taking the entire global economy over the cliff.

No wonder the ranks of capitalism’s critics continue to swell, as does the vehemence of their critiques. No wonder more young people now say they prefer socialism to capitalism (43 per cent to 32 per cent).[17] No wonder the communications group Edelman reported recently that the credibility of corporate CEOs has fallen ‘off a cliff’, dropping 12 points in just the past year.[18]

A better way

There is a better way. Business, practised wisely and well, is an extraordinarily powerful means for human betterment. Business fulfils this high calling by creating value for its stakeholders in two particular and important ways. First and foremost, business solves human problems. In fact it solves an especially large and important set of human problems: the material challenges of human existence.

Virtually every product and service offered by business is meant to meet a material human need.[19] In some cases business products may represent novel and dramatic new solutions to those needs (breakthroughs), as happened with the invention of automobiles, personal computers and mobile phones. In other cases the solutions may be more modest: a less expensive option for air travel, a more comfortable mattress or a non-polluting laundry detergent. All of which makes business, quite literally, a solutions machine targeted at humankind’s material welfare.

But business creates an entirely different type of value as well. When a business sells its products for more than their cost of production, it creates profit – and thereby enlarges human wealth. Provided this wealth is broadly deployed rather than narrowly hoarded, business both solves human problems and creates the economic provision that makes those solutions affordable and accessible.

Both forms of value creation are extraordinarily important. As Eric Beinhocker and Nick Hanauer note in their compelling article, ‘Capitalism Redefined’: ‘Ultimately, the measure of a society’s wealth is the range of human problems that it has found a way to solve and how available it has made those solutions to its citizens.’[20] It is no overstatement, therefore, to say that business provides the material foundation for human flourishing.

Or, more precisely, business is capable of providing the material foundation for human flourishing. It delivers these great benefits when, and to the degree that, it engages in win–win behaviour. Period. But win–lose behaviour is an entirely different matter. When business selfishly and narrow-mindedly pursues profits at the expense of stakeholders, then it becomes something altogether disparate. Rather than a means of value creation, it becomes a mechanism for value extraction – in other words, for plunder and stealing. That version of business – based on the intrinsically selfish ideology of shareholder value maximisation – rightly deserves the ire and condemnation increasingly directed against it.

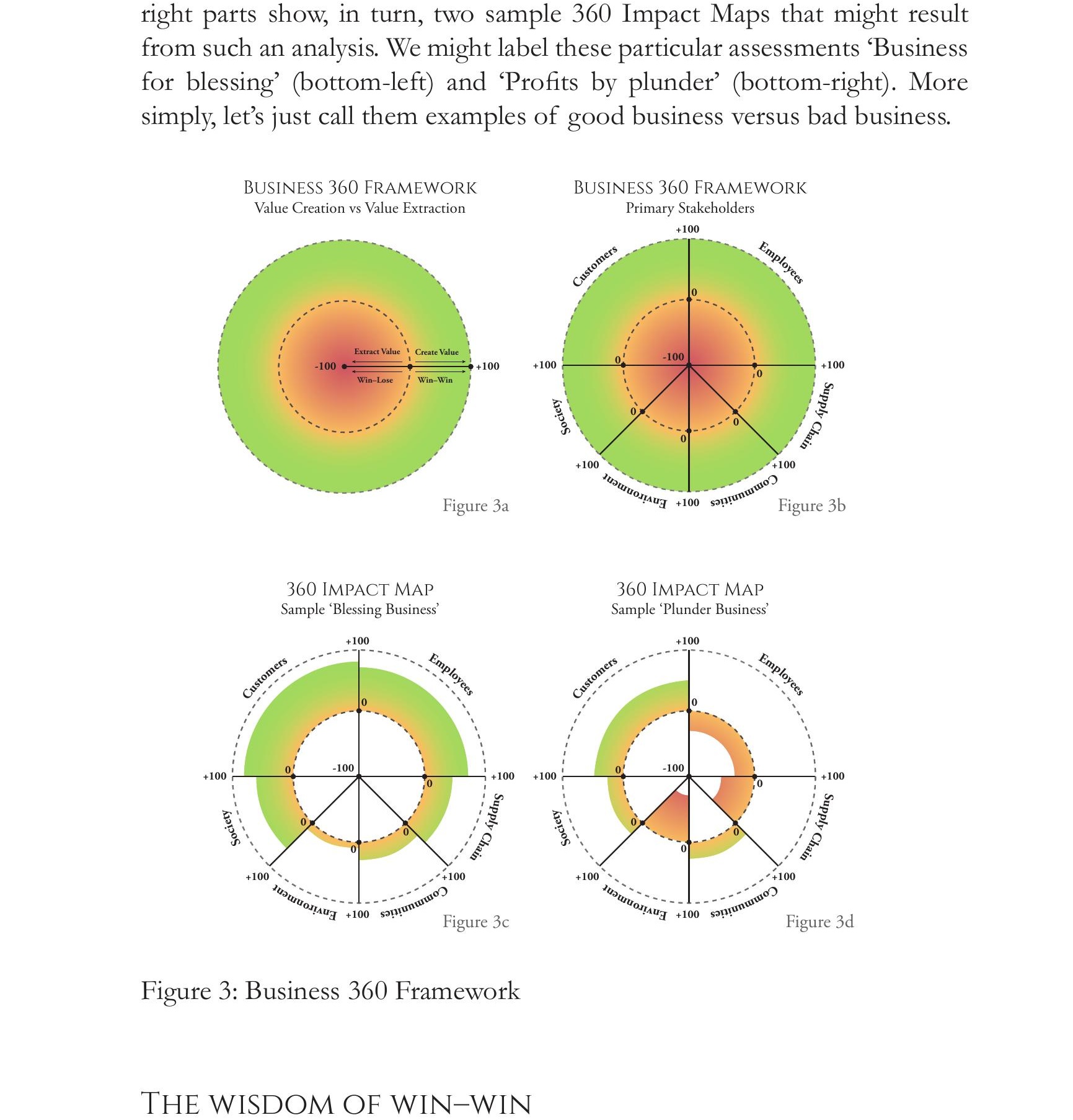

The Business 360 Framework[21] provides a helpful analytical tool by which to understand and apply all this in practice, as shown in Figure 3. The top-left part of this figure identifies the crucial difference between win–win behaviour that creates value for stakeholders, versus win–lose behaviour that extracts value, and provides a +100 to -100 reference scale. The top-right part lays the basis for applying this create-versus-extract value assessment to each of a company’s primary stakeholders. The bottom-left and bottom-right parts show, in turn, two sample 360 Impact Maps that might result from such an analysis. We might label these particular assessments ‘Business for blessing’ (bottom-left) and ‘Profits by plunder’ (bottom-right). More simply, let’s just call them examples of good business versus bad business.

The wisdom of win–win

Is good business too much to ask? Hardly. First off, it’s the way business was characteristically practised until recently, including during its (American) mid-twentieth-century heyday. Second, it asks business to forsake neither self-interest nor the pursuit of profit. It simply requires that business not pursue self-interest and profit in ways that harm others. How is that unreasonable? (And what argument would business make as to why it should be allowed to inflict harm on others?)

More importantly, win–win behaviour is in the best interest of business. Treating others the way we want to be treated is the only behaviour that really works. It’s the behaviour that creates trust and fosters relationship. These are the essential building blocks of sustainable business success – trust and relationship with customers, with employees, with suppliers and so on. In fact without trust and relationship, business grinds to a halt.

It’s not surprising, then, that the empirical evidence for golden-rule behaviour in business is compelling. In The Ultimate Question, first published in 2006, Fred Reichheld introduced the powerful new business metric Net Promoter Score (NPS). Superficially, NPS measures how well or poorly a company satisfies its customers. But according to Reichheld, what NPS really measures is golden-rule behaviour. In turn, Reichheld marshals compelling data demonstrating that companies with superior NPS scores have substantially higher rates of profitability and growth than their competitors.

Similarly, in her 2013 book The Good Jobs Strategy, Zeynep Ton, one of the foremost retail operations experts, makes a powerful empirical case that – even in the extremely price-sensitive arena of low-cost retail – the most successful companies are the ones that pay and treat their workers well. Specifically, she found that these ‘good jobs’ companies were anywhere from 50 to 300 per cent better than their competitors at bottom-line performance metrics such as inventory turns, sales per employee and sales per square foot.

Let’s complement this with some anecdotal evidence:

Isadore Sharp, founder and chairman of the Four Seasons hotel group: ‘Our success all boils down to following the golden rule.’

Colleen Barrett, retired president of Southwest Airlines: ‘Practising the golden rule is integral to everything we do.’

Andy Taylor, CEO of Enterprise: ‘golden rule behaviour is the basis for loyalty. And loyalty is the key to profitable growth.’[22]

John Bogle, founder and former CEO, Vanguard Group: ‘You [only need] one rule … “Do unto others as you would have them do unto you.”‘[23]

The ‘golden rule’ is called that for a reason. Throughout human history it has been the gold standard for good behaviour. And for prudent behaviour. Profiting at the expense of others may work in the short term but not in the long. The merchant who delivers good value can expect to operate indefinitely; not so the knife-wielding mugger. Or as Jim Collins says in his seminal book Built to Last: ‘You can cheat your way to seeming greatness for five or ten years, but not for fifty or one hundred years.’[24]

It’s high time, therefore, for American public company CEOs to give up their profits-by-plunder myopia; high time to forsake win–lose value extraction and recommit to win–win value creation for all stakeholders. It’s how capitalism was always meant to work – for everyone.

Notes to Chapter 4

[1] Edward L. Glaeser, ‘Can Business Do Well and Do Good?’, The New York Times, 6 January 2009; emphasis added.

[2] From Quote Investigator: Exploring the Origins of Quotations, http://quoteinvestigator.com/2011/02/23/capitalism-motives.

[3] From Quote Investigator: Exploring the Origins of Quotations, http://quoteinvestigator.com/2011/02/23/capitalism-motives.

[4] https://en.wikipedia.org/wiki/The_Virtue_of_Selfishness.

[5] Transcript of Milton Friedman interview quoted in ‘Donald Trump Says Greed Is Good’, by Aaron Sandler, The Daily Wire website.

[6] Which is not to say the divide between selflessness and self-interest is unimportant. It has considerable significance related to one’s character growth and spiritual development. But as regards outcomes, and the difference between right and wrong, moral and immoral, the dividing line of real consequence is between win–win mutuality and win–lose selfishness and predation.

[7] Mark Skousen, The Big Three in Economics: Adam Smith, Karl Marx, and John Maynard Keynes, Armonk, NY and London: M. E. Sharpe, 2007, p. 29.

[8] Mark Skousen, ‘Is Greed Good?’, Foundation for Economic Education, 1 May 2001; emphases in first paragraph added; emphasis in second paragraph original.

[9] Adam Smith, The Theory of Moral Sentiments, II.ii.2.

[10] In her excellent book The Shareholder Value Myth, the respected Cornell Law School professor Lynn Stout makes a convincing case that neither shareholders nor anyone else are the legal owners of corporations. That said, whatever their precise legal status, in the shareholder-centric version of business embraced in the USA since the 1980s, shareholders are clearly the effective and beneficial owners of public corporations – Lynn Stout, The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the Public, San Francisco, CA: Berrett-Koehler, 2012.

[11] Reprinted in Walther Ch. Zimmerli, Markus Holzinger and Klaus Richter (eds), Corporate Ethics and Corporate Governance, Heidelberg: Springer, 2010, pp. 173–8.

[12] Michael C. Jensen and William H. Meckling, ‘Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure’, Journal of Financial Economics 3:4, 1976, pp. 305–60.

[13] John F. Welch, ‘Growing Fast in a Slow Economy’, speech to financial community representatives, Hotel Pierre, New York, 8 December 1981.

[14] In fact it disadvantages long-term shareholders as well. A major study from the Harvard Business School, ‘Competitiveness at a Crossroads’, February 2013, comes to the blunt assessment that American business is losing the ability to compete in the global marketplace. Much of this is driven by companies’ squeezing research and development budgets to maximise short-term profits and fund dividend payments and stock buybacks.

[15] This chart comes from Andrew Smithers, economist and founder of Smithers & Co. Until recently he also wrote a recurring column for the Financial Times. The chart can be found at www.pbs.org/newshour/making-sense/merle-hazard. To be clear, SVM has not been the only driver of the disproportionate flow of business rewards towards owners and away from workers during the last few decades. Globalisation and automation have also had significant effect. Without the embrace of SVM, however, business would have looked for ways to mitigate the anti-worker effects of these other factors. Instead, SVM justified a wholesale embrace of any measures that fattened profits at the expense of workers and/or other stakeholders.

[16] ‘The Low-Wage Drag on Our Economy: Wal-Mart’s Low Wages and their Effect on Taxpayers and Economic Growth’, a report from the Democratic Staff of the US House Committee on Education and the Workforce, May 2013.

[17] Catherine Rampell, ‘Millennials Have a Higher Opinion of Socialism than of Capitalism’, The Washington Post, 5 February 2016.

[18] 2017 Edelman Trust Barometer: Global Annual Survey, 15 January 2017, www.edelman.com/trust2017.

[19] That said, it should be acknowledged that some businesses meet ‘needs’ that many may judge to be illegitimate – such as pornography or gambling.

[20] Nick Hanauer and Eric Beinhocker, ‘Capitalism Redefined’, Evonomics, 30 September 2015 – http://evonomics.com/redefining-capitalism-eric-beinhocker-nick-hanauer; originally published in Democracy: A Journal of Ideas, 31, Winter 2014 – http://democracyjournal.org/magazine/31/capitalism-redefined/?page=all.

[21] Developed by Eventide Asset Management, LLC as a guiding framework for ‘better investing for a better world’.

[22] All three quotations are from Fred Reichheld with Rob Markey, The Ultimate Question 2.0: How Net Promoter Companies Thrive in a Customer-Driven World, Boston, MA: Harvard Business School Publishing, 2011.

[23] John C. Bogle, ‘What I’ve Learned in a Half Century in Business – Twelve Rules For Building A Great Work Force’, 23 April 2003, www.vanguard.com/bogle_site/sp20030423.html.

[24] James C. Collins and Jerry I. Portas, Built to Last: Successful Habits of Visionary Companies, New York: HarperBusiness, 1994, p. xi.